Is RBI’s New Plan for Bad Loans Just Another Quick Fix?

In a country like India, where millions hover between poverty and fragile middle-class dreams, every bad loan is more than a financial misstep – it's a broken promise. The Reserve Bank of India’s (RBI’s) latest fix for India’s non-performing assets (NPA) crisis, securitisation of stressed assets, may sound bold but it risks papering over deeper cracks.

By pushing banks to bundle and sell bad loans as securities, it sidesteps the root problem: how these loans piled up in the first place. Bad loans don’t just distort balance sheets – they block credit flow, deepen inequality and erode public trust in the financial system.

We need solutions, not another shortcut.

Globally, India stands out as an outlier in bad loans, with an average NPA ratio of 6.1% from 2010 to 2022, peaking at nearly 10% in 2017 – among the highest in the world, according to World Bank data. In contrast, China maintained 1%, Japan kept levels consistently low, while the US, the UK, Brazil and South Africa saw far more stable trends. This underscores the severity of India’s banking crisis and the urgent need for lasting reforms.

RBI’s recent move seeks to repurpose bad loans into tradable securities, offering a market-led solution. But will this new approach lead to a long-term sustained measure or will just provide short-term relief?

A Brief History of India’s Bad Loan Problem

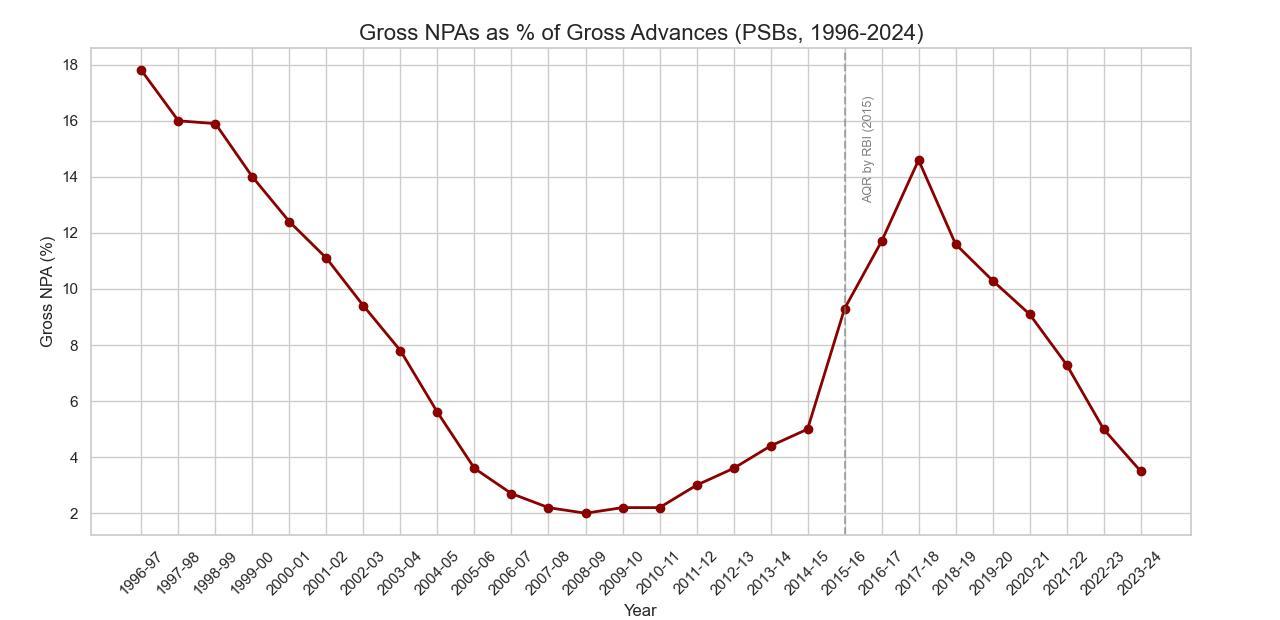

India’s NPA crisis took root post-liberalisation. Following the Narasimham Committee Report (1991) and the introduction of prudential norms in 1992-93, public sector banks (PSBs) disclosed gross NPAs at 25% of gross advances by 1994. Between 2005-2013, NPAs stayed low due to high growth and credit expansion.

However, the RBI’s 2015 asset quality review revealed deep stress, pushing the PSB NPA ratios to 14.6% by 2017-18. Despite write-offs, insolvency and bankruptcy code (IBC) resolutions, and recapitalisation, the problem persists. As of March 2024, banks hold Rs 4.8 lakh crore in gross NPAs – 71% (Rs 3.39 lakh crore) alone from PSBs.

Source: Trends and Progress of Banking in India, Reserve Bank of India; and Database on the Indian Economy, Reserve Bank of India

The birth of bad debt: NPA sources

The nature and sources of India’s bad loans have shifted significantly over time. In 1994-95, priority sector loans accounted for 50% of PSBs' NPAs, while non-priority sectors made up 47%. By 2014-19 – when NPAs peaked – this reversed: priority sector NPAs fell to 26%, while non-priority sector NPAs surged to 74%. This shift coincided with the RBI’s asset quality review, which revealed deep stress in infrastructure lending, especially in the power sector (60% of total infra credit).

Borrower-related issues like poor appraisal, over-leveraging, evergreening, fund diversion and weak management worsened the crisis. Delays in infra projects, monsoon-reliant agriculture, and growing Non-Banking Financial Company (NBFC) exposure (2% in 2005 to 9% in 2024) have added fragility. The IL&FS collapse showed how NBFC risks can spill over. Another red flag was when PSBs’ exposure to sensitive sectors like capital markets and real estate rose 24-fold since 2005 to Rs 20.98 lakh crore. As of March 2024, 22.1% of PSB and 34.7% of private bank loans are tied to these volatile sectors.

The Human Cost of NPAs

Bad loans don’t just weaken banks – they hurt the entire economy. As banks set aside large provisions from their profits to cover future losses, their ability to lend shrinks, especially to farmers, small businesses and the middle class.

This leads to stalled, labour-intensive projects, job losses and restricted social mobility. Government bailouts to recapitalise banks widens the fiscal deficit, which in turn is used to justify subsidy cuts or tax hikes – fuelling inflation and deepening inequality.

Every rupee spent rescuing banks is a rupee diverted from healthcare, education and jobs. Worse, when large corporate defaulters walk free while small borrowers are penalised, it erodes public trust in the banking system and in the rule of law.

Debt recovery or debt evasion?

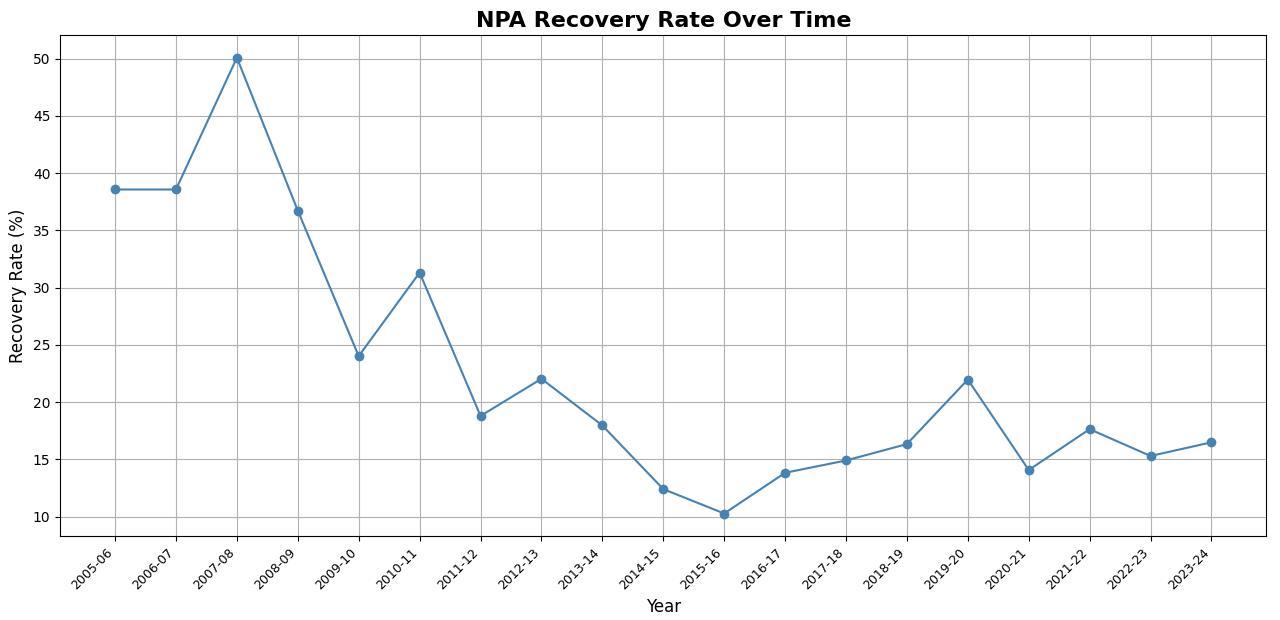

India’s bad loan recovery record reveals deep systemic flaws. Recovery peaked at 50.1% in 2007-08 but plunged to 10.3% in 2015-16, and only modestly improved to 16.5% by 2023-24. Under the IBC, banks recover just 23% of claims, with resolution taking an average of 679 days – far beyond the mandated 330 days.

The NCLT is overburdened, debt recovery tribunals are understaffed, and SARFAESI remains inconsistently enforced. Haircuts as high as 85% raise moral hazard concerns. Of 7,567 CIRP ( Corporate Insolvency Resolution Process) cases, 72.3% ended in liquidation, while only 27.7% saw resolution.

Financial creditors recovered just 34.36% & operational creditors just 10.7%. The amount forgone – write-offs or loans that banks failed to recover – rose from Rs 11,600 crore in 2005–06 to Rs 4.87 lakh crore in 2023–24.

In the last decade alone, banks wrote off Rs 16.35 lakh crore, recovering only a fraction. Reduced NPA levels now reflect write-offs, not real recoveries, while those responsible for reckless lending face no consequences.

Source: Trends and Progress of Banking in India, Reserve Bank of India; and Database on the Indian Economy, Reserve Bank of India

Source: Trends and Progress of Banking in India, Reserve Bank of India; and Database on the Indian Economy, Reserve Bank of India

Calculation: Amount Forgone = NPA Amount Involved - Amount Recovered

India’s banking sector faces deep-rooted issues worsening the NPA crisis. Despite a low credit-to-GDP ratio (56%), India has one of the highest NPA ratios, reflecting weak credit assessment. But the issue runs deeper.

Ever-greening of loans, skewed credit flows to large corporates, and high PSB provisioning further erode transparency, capital strength, and inclusive lending.

“Credit by banks is always a calculated risk which bankers take and there are chances of NPAs. But it is important to determine what kind of NPAs we are dealing with. For instance, even if many small loans go bad, the banks’ balance sheets are not affected. But when one large credit goes bad, when one big corporate defaults, the balance sheets are affected”, says Thomas Franco, the former general secretary of the All India Bank Officers’ Confederation (AIBOC).

“So, the focus of credit needs to change,” he says, adding, “RBI should implement its own decision of restricting credit to one corporation to Rs 10,000 crore by all banks. They should be asked to mobilise funds from the market.”

Source: RBI, Statistical Tables Relating to Banks of India

RBI’s new move: Securitisation of stressed assets

The RBI’s recent draft guidelines on NPAs, titled ‘Securitisation of Stressed Assets’, propose that banks bundle stressed loans into marketable securities and sell them to investors. This aims to ease balance sheet pressure and unlock market-driven solutions for bad loan recovery, complementing existing mechanisms like ARCs, IBC and NCLT.

The RBI intent sounds good, allowing greater participation from resolution experts and ensuring transparency through disclosures, independent valuations and pricing norms. However, concerns persist. A key issue is the overreliance on credit rating agencies (CRAs).

Ratings will influence capital requirements for banks but past failures like IL&FS and DHFL show how CRAs can overstate recovery potential. Incorrect ratings could result in banks holding insufficient capital, risking systemic instability.

Another problem is that banks may not be required to retain a share in the stressed loans they sell, potentially leading to careless asset transfers with no incentive for recovery. Additionally, important categories such as fraud, wilful defaults, farm and student loans are excluded, limiting the framework’s reach.

Operational complexity is another challenge. With multiple players involved – banks, special purpose entities, servicers, and resolution managers (ReMs) – coordination sometimes may become messy. Allowing originator banks to act as ReMs creates a potential conflict of interest: Will they prioritise recovery or simply clean their books? If investor demand is weak, this could become more of a balance-sheet trick than a true resolution mechanism.

The RBI’s move marks a shift from state-led bailouts to market-based resolutions. But given the past experience with Asset Reconstruction Companies and NCLTs, there is still no certainty that recovery will be prioritised and it simply won't be a balance sheet exercise.

Success thereby will depend on regulatory clarity, enforcement and public trust. Strengthening credit appraisal norms, risk-based sectoral exposure limits, time-bound out-of-court restructuring and granting PSBs operational autonomy could be the real reforms that can effectively deal with NPAs.

After all, cleaning up bad loans isn't just about financial housekeeping – it’s vital for restoring the public’s faith in the banking system.

Pranay Raj works as a Data Analyst at the CFA, New Delhi.

This article is written in collaboration with the All India Bank Officers’ Confederation.

This article went live on May twenty-fourth, two thousand twenty five, at fifty-three minutes past four in the afternoon.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.