How Stalled Projects, Cost Overruns and Delays in Policy Approvals Fuel the NPA Crisis

This is the second part of a two-part series outlining the nature of macroeconomic and financial challenges in front of the new RBI governor, Sanjay Malhotra. Read the first part here.

In addition to some of the macroeconomic issues highlighted in the earlier part, the new Reserve Bank of India (RBI) governor may need to also closely observe India’s banking sector which has wrestled with the challenge of Non-Performing Assets (NPAs) for over a decade and a half now. While overall NPA levels have improved in recent years, thanks to increasing write offs (which present its own set of challenges-discussed here), much of the financial data reveals that much of the burden continues to rest on Public Sector Banks (PSBs).

Simultaneously, sectoral challenges seen in agriculture, MSMEs, and manufacturing highlight systemic weaknesses, which, if left unaddressed, could jeopardise long-term financial stability and keep India’s growth cycle at a sub-optimal level. The observed trends, particularly between 2019-20 and 2022-23, reflect both progress and the need for targeted policy interventions.

According to data from the RBI annual report, PSBs saw their gross NPAs decline significantly from Rs 6.78 lakh crore in 2019-20 to Rs 4.35 lakh crore in 2022-23, reflecting efforts like recapitalisation, asset resolution, and stricter lending guidelines. Meanwhile, Private Sector Banks (PVBs) reported a more modest decline, with gross NPAs falling from Rs 1.83 lakh crore to Rs 1.15 lakh crore during the same period. This difference underscores the systemic weaknesses in public banks, which have historically been more exposed to priority sector loans and large-scale corporate lending.

While the decline in NPAs signals improvement, challenges persist, especially in agriculture, MSMEs, and manufacturing. The sharp rise in NPAs for Small Finance Banks (SFBs) – from Rs 1,709 crore in 2019-20 to Rs 8,869 crore in 2022-23 – further reflects the growing stress in niche financial institutions, which cater predominantly to small borrowers.

Agriculture: Persistent Stress Despite Loan Waivers

Agriculture, a critical component of India’s economy, continues to face rising NPA levels, particularly in PSBs. Between 2019-20 and 2022-23, agricultural NPAs in PSBs increased from Rs 1.11 lakh crore to Rs 1.14 lakh crore. This modest increase masks underlying structural challenges such as loan waivers, price volatility, and inadequate insurance mechanisms. While farm loan waivers provide short-term relief, they erode repayment discipline and weaken bank balance sheets.

Source: Author’s Calculations | RBI Statistics

The government has introduced initiatives like the Pradhan Mantri Fasal Bima Yojana and PM-Kisan Samman Nidhi to address financial stress in the agriculture sector. However, systemic issues remain. According to an analysis by The Hindu market access, coupled with uneven credit distribution, continues to exacerbate defaults. To address agricultural NPAs, policy solutions must go beyond loan waivers, focusing instead on improving crop insurance, stabilising prices, and enhancing rural infrastructure.

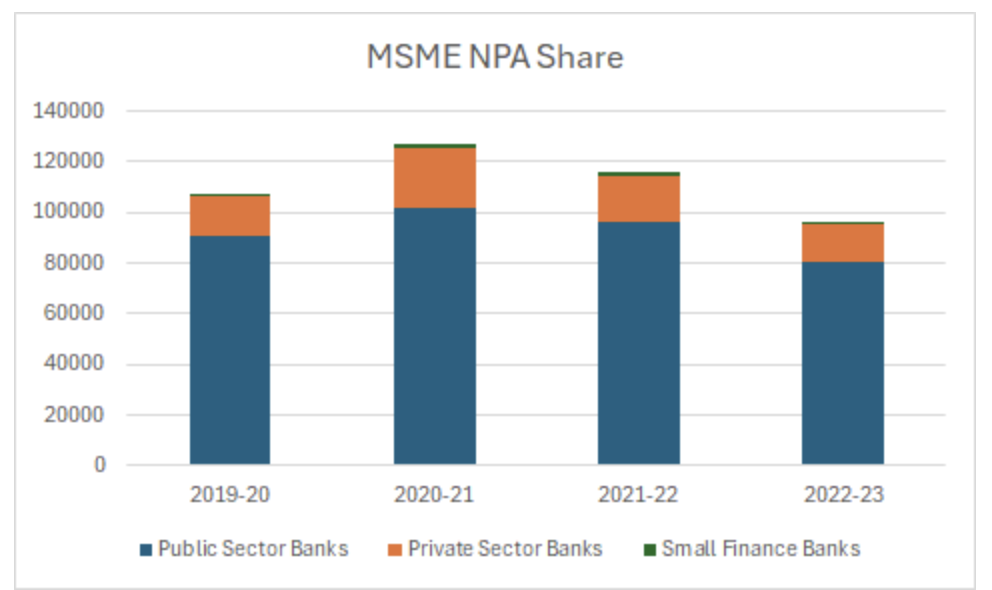

MSMEs: Falling NPAs but continued credit crunch

The MSME sector, which contributes nearly 30% of India’s GDP and provides employment to millions, showed a decline in NPAs between 2019-20 and 2022-23. Public Sector Banks reported a reduction from Rs 90,769 crore to Rs 80,577 crore during this period. This improvement can be attributed to targeted government interventions such as the Emergency Credit Line Guarantee Scheme (ECLGS), launched to support MSMEs during the pandemic.

Source: Author’s Calculations | RBI Statistics

Despite this progress, MSMEs continue to face systemic challenges. According to Economic Times, MSMEs struggle with limited working capital, delayed payments from large corporations, and slow demand recovery post-pandemic. While the introduction of the Udyam registration portal has brought many MSMEs into the formal credit system, a significant gap remains in access to timely and affordable credit.

The pandemic exacerbated financial stress for small businesses, and while restructuring programs have provided temporary relief, the long-term solution lies in improving cash flows, ensuring faster payment settlements, and providing targeted credit guarantees to MSMEs.

Manufacturing: The Largest Contributor to NPAs

The manufacturing sector remains the largest contributor to NPAs in India, particularly in PSBs. Over the years, large corporate defaults have continued to plague the sector, with companies like Bhushan Power and Steel defaulting on loans exceeding Rs 41,400 crore. Similarly, firms in the power sector, such as KSK Mahanadi Power Company, owed over Rs 21,390 crore, reflecting systemic failures in risk assessment, project implementation, and recovery mechanisms.

Source: Author’s Calculations | RBI Statistics

The manufacturing sector’s NPA crisis is closely tied to stalled projects, cost overruns, and delays in policy approvals. The power sector, for example, has suffered from weak demand and low capacity utilisation, rendering many projects unviable.

The Insolvency and Bankruptcy Code (IBC), introduced in 2016, was designed to streamline the resolution of stressed assets. While the IBC has improved recovery rates, delays in the insolvency process continue to limit its effectiveness. According to the Insolvency and Bankruptcy Board of India (IBBI), the average recovery rate under the IBC stands at 30-35%, leaving banks with substantial losses.

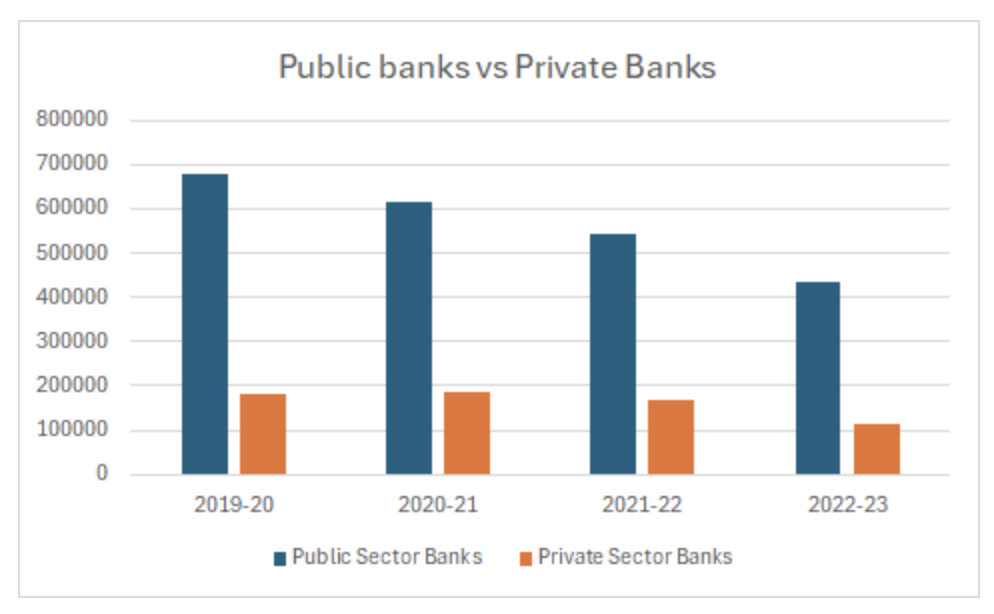

Private Banks vs Public Banks: A tale of two strategies

The contrasting trends between PSBs and PVBs highlight differences in their lending practices and risk management strategies. While PSBs remain heavily exposed to priority sectors and large industrial loans, private banks have focused more on retail lending and small businesses, which carry lower default risks. This difference is reflected in the NPA data:

Source: Author’s Calculations | RBI Statistics

- Public Sector Banks: Declined from Rs 6.78 lakh crore in 2019-20 to Rs 4.35 lakh crore in 2022-23.

- Private Sector Banks: Reduced NPAs from Rs 1.83 lakh crore to Rs 1.15 lakh crore during the same period.

The ability of private banks to maintain lower NPA levels highlights their focus on better risk assessment, stricter credit discipline, and higher recovery rates. In contrast, PSBs, which are more exposed to politically sensitive sectors like agriculture and large-scale manufacturing, face greater systemic challenges.

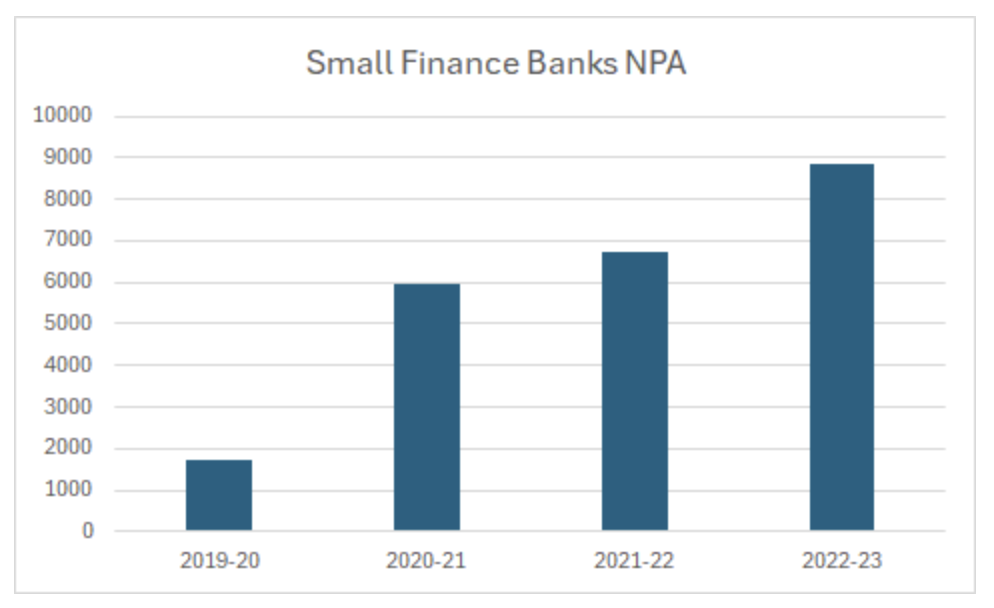

SFBs, which cater to underserved and small borrowers, have seen a sharp rise in NPAs, jumping from Rs 1,709 crore in 2019-20 to Rs 8,869 crore in 2022-23.

Source: Author’s Calculations | RBI Statistics

The surge in defaults reflects the economic vulnerability of small borrowers, particularly during the pandemic. While SFBs play a crucial role in financial inclusion, their rising NPAs highlight the need for stronger borrower assessment frameworks and risk management practices.

Addressing the chronic NPA challenge

India’s NPA problem has undoubtedly improved in recent years, but the data highlights persistent sectoral vulnerabilities. The manufacturing sector, with its large-scale defaults and stalled projects, remains the single largest contributor to NPAs. Meanwhile, agriculture and MSMEs, which are critical to India’s economy, continue to face financial stress, particularly in PSBs. The rise in NPAs for SFBs further underscores the need for a robust credit assessment framework.

Also read: Narendra Modi's Mammoth Bank Heist Over the Last 10 Years

Resolving India’s NPA crisis requires a multi-pronged approach – strengthening the Insolvency and Bankruptcy Code to expedite recoveries, improving risk assessment practices, and ensuring greater accountability in loan write-offs are essential steps. For sectors like agriculture and MSMEs, targeted policy measures – including better price stabilisation, timely payments, and credit guarantees – can help address structural weaknesses.

While the decline in NPAs among private banks signals progress, PSBs, at the direction of the RBI, must implement stricter credit discipline and project monitoring mechanisms to reduce their exposure to risky loans. Greater transparency in the increasing trend of loan write-offs and a focus on recovering dues from large defaulters will be key to restoring confidence in India’s banking system.

Deepanshu Mohan is a professor of economics, dean, IDEAS, and director, Centre for New Economics Studies. He is a visiting professor at the London School of Economics and an academic visiting fellow at AMES at the University of Oxford.

Aryan Govindakrishnan is a senior research analyst with Centre for New Economics Studies (CNES), O.P. Jindal Global University.

This article went live on January third, two thousand twenty five, at thirty minutes past six in the evening.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.