Mumbai: Credit research firm CreditSights has red-flagged the Adani Group’s over-leveraged expansion bid vis-a-vis the Reliance conglomerate. In a research note, the credit research firm raises the worst-case scenario possibility of the group’s “overly-ambitious debt-funded growth plans” eventually spiralling into a massive debt trap, and possibly culminating in a distressed situation or default of one or more group companies.

The report puts the spotlight on several weighty financial concerns that besiege the Adani Group and have worried market analysts and shareholders across the board.

The credit report has drawn up a number of credit concerns ranging from the group’s overly-leveraged aggressive expansion to forays into new or unrelated businesses, environmental, social and governance (ESG) risks, risks emanating from competing with the likes of Reliance Industries and, last but not least, limited evidence of equity capital injections by Gautam Adani and his family.

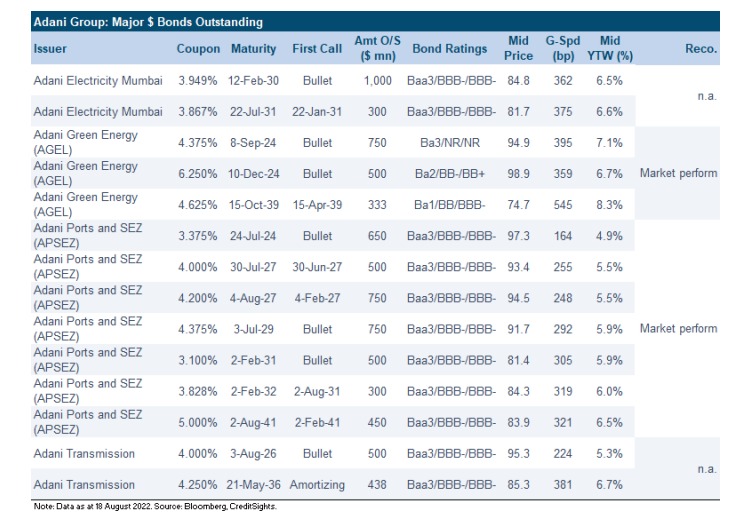

After the Reliance and Tata groups, the Adani Group is the third largest conglomerate in India based on a total market capitalisation of over $200 billion, as of August, 2022. Founded in 1988 as a commodity trading business by businessman Gautam Adani, the Group has expanded rapidly across key industry verticals such as energy, utilities and transportation. The Group has six established listed entities, namely Adani Enterprises (AEL), Adani Green Energy (AGEL), Adani Ports and Special Economic Zone (APSEZ), Adani Power, Adani Total Gas and Adani Transmission.

Also read: The Adani Juggernaut Is Expanding on All Fronts, Australian Coal Need Not Be One of Them

While marking out that CreditSights remains “cautiously watchful” of the Adani Group’s largely debt-funded expansion appetite, the report states:

“In general, the group has been investing aggressively across both existing and new businesses, predominantly funded with debt, resulting in elevated leverage and solvency ratios. This has understandably caused concerns about the group as a whole, and what implications it could have on the group companies that are bond issuers. In the worst-case scenario, overly ambitious debt-funded growth plans could eventually spiral into a massive debt trap, and possibly culminate into a distressed situation or default of one or more group companies.”

It goes on to add that the rapid expansion has largely been fuelled by debt funding which has caused “the leverage (gross or net debt/EBITDA) of several Group companies and hence, of the overall consolidated group, to soar in the past few years.” EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortisation

“Excessive debt and overleveraging by the Group,” the report states, “could have a cascading negative effect on the credit quality of the bond issuing entities within the group and heightens contagion risk in case any entity falls into distress.”

Below, each one of the concerns red-flagged by CreditSights is taken up in greater detail.

Foray into new businesses and forceful expansion of existing businesses

The report states the group has been expanding in virtually all of its businesses and has been rapidly expanding operations in its existing businesses, as is the case with Adani Green which is aiming to grow its operational renewable capacity almost five-fold by FY25.

The group is also planning on venturing into sectors where it has no prior experience or expertise, which includes domains like copper refining, petrochemicals, data centres and most recently, telecom and aluminium production. CreditSights also points out that the Adani Group became the second largest cement maker “virtually overnight” by acquiring Holcim’s controlling stake in Ambuja Cement and ACC Limited for $10.5 billion.

Also read: The ‘Cartelisation’ of the Indian Cement Industry: Antitrust Report

A majority of the businesses running under the aegis of the Adani Group are capital intensive and require large investments and constant funding in the initial years, as well as in the following years, considering that these projects have long gestation periods.

Most of the projects/ventures are mostly funded by borrowings (typically in the ratio of 3:1 debt/equity). In India, typical borrowing costs for infrastructure projects are as high as 9-11% per annum (depending on domestic benchmark rates), which adds a large interest burden on the entities.

Further, considering the businesses do not make profits in the initial few years, they typically don’t have the ability to repay the debt immediately and rely on rolling over/refinancing the obligations in the initial few years, which is, in turn, dependent on maintaining solid banking relationships and on strong capital market conditions.

The report, after citing the challenging conditions in the Indian ecosystem, goes on to warn:

“Despite elevated leverage levels and poor interest cover (due to past expansion and the capital-intensive nature of the projects, funded largely with debt), virtually all Adani Group companies have large expansion plans on the horizon too, having adopted aggressive growth targets; which is not a financially prudent strategy.”

Spotlight on Adani Enterprises Limited

Given that Adani Enterprises Limited is the primary incubator for new and developing businesses, AEL incurs the highest capital expenditure (CapEx) cost among group companies. In the last five years, the company has invested heavily in new growth sectors that include airports, cement, copper refining, data centres, green hydrogen, petrochemical refining, roads and solar cell manufacturing. Looking ahead, it plans to foray into the enterprise data in telecom and has massive plans to grow its green hydrogen and airport businesses.

“These ventures are also extremely capital intensive (as seen from the table above), which would likely increase the need for additional debt incurrence to fund the CapEx needs and thus leading to sustained high leverage for the group,” the report explains.

Limited evidence of equity capital injections

Equity infusions by the key promoter, Gautam Adani and his family, are not common in the Adani Group. Generally, the Adani family injects equity mainly into its newer businesses (which are all housed under AEL). Once they are more sustainable, they are hived off to run independently, mostly by listing them on the stock exchange. Thereafter, the businesses are largely reliant on bank loans, internal accruals (i.e. operating cash flows) and debt capital market funding.

The report mentions the astronomical rise of Gautam Adani’s wealth and his recent feat of displacing Bill Gates to occupy the position of the fourth-richest man in the world. However, it cuts a sour note for Gautam Adani by adding, “this is paper wealth, and largely tied to the value of his holdings in the Adani Group’s stocks, which have risen significantly in recent years. It is difficult to gauge the family’s ability to inject their own funds in a scenario where any of the Group companies require equity injections by the promoter.”

The report also mentions governance risks: “Since the 6 listed Group companies are separate legal entities, the provision of inter-company loans by a performing company to its stressed sister entity would be a related-party transaction and raise corporate governance issues.”

Vying with Reliance Industries

CreditSights highlights the rivalry brewing between the two marquee Indian conglomerates. While Adani Green Energy Limited entered the renewable energy business in 2015, RIL also announced its foray into the sector in 2021. Conversely, Reliance was a new entrant in the telecom market in 2015 whereas Adani followed into the telecom business by successfully bidding for spectrum in India’s recently-held 5G auctions.

Mukesh Ambani, chairman and managing firector of Reliance Industries, gestures as he answers a question during a media interaction in New Delhi, India, June 15, 2017. Photo: Reuters/Adnan Abid

While the Adani group had clarified that it is not eyeing the commercial consumer telecom business, the report accounts for the fact that the possibility of the Adani Group taking a leap into the telecom sector cannot be ruled out.

“As the two mega conglomerates in the Indian corporate sector compete for market share in a few new economy businesses (e.g., renewable power, telecom), it could lead to some imprudent financial decisions from both sides, such as higher CapEx spends, aggressive bidding, and over-leveraging. On the whole, RIL has been on a de-leveraging trend over the past few years and boasts robust credit metrics (gross and net leverage at 2.6x and 2.2x as of end-FY22) and interest cover (7.8x at FY22). On the other hand, as highlighted above, Adani has elevated leverage and poor interest cover and cash outflows across virtually all its entities, and is at greater financial risk.”

Governance risks

Some foreign investors in Adani Group stocks also include certain opaque funds, such as Albula Investment Fund, Cresta Fund and APMS Investment Fund, all of which are registered at the same address in Port Louis, Mauritius.

The majority of these funds’ assets under management (AUM) is in Adani Group stock and there is little clarity regarding the ultimate, beneficial owner of these funds. Though there was news last year regarding the stock regulator, the Securities and Exchange Board of India (SEBI) investigation for alleged stock price manipulation, SEBI has since cleared the Adani Group companies of any potential irregularities.

A shareholding structure dominated by the Promoter Group and foreign portfolio investors, some of which are quite opaque, along with minimal equity research coverage by sell-side banks (whether local or foreign), is quite unusual for such large-cap stocks.