Jet Airways’ Bumpy Flight Path Points to Serious Issues with India’s New Bankruptcy Code

This is part one in a two-part series on how Jet Airways show the ways in which India's new bankruptcy code is inadequate. Read part two here.

On November 10, 2022, came startling news.

As a part of an investigation into suspected fraud and money laundering, prosecutors in Liechtenstein, Switzerland and Austria had raided multiple properties belonging to Florian Fritsch. The investigation was based, said the Liechtenstein prosecutor, on "several complaints by suspected victims".

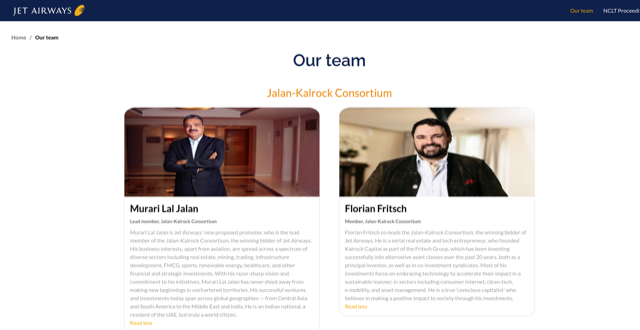

The news created ripples in distant India. Fritsch is the promoter of Kalrock Capital Partners which, along with UAE-based businessman Murari Lal Jalan, has bought Jet Airways through bankruptcy proceedings.

Kalrock was quick to dismiss any suggestions of impropriety. “The investigation...has been initiated based on anonymous complaints filed in relation to certain businesses where Florian is one of the financial investors in his personal capacity,” it said, adding the disputes are “commercial in nature”.

The firm also said neither it nor Jet had any connection with these charges. “These investigations have no impact (on) the acquisition of Jet Airways, and Jalan-Kalrock Consortium remains committed towards Jet Airways,” it said.

Kalrock’s statement notwithstanding, the raid underscored how poorly Jet Airways’ tryst with bankruptcy proceedings is progressing.

Once India’s leading airline, Jet entered bankruptcy courts in April, 2019, after attempts to save it failed. Its resolution process saw established firms in the aviation sector drop out early and a bevy of unknown firms, like Russia’s Treasury RA Creator, throw their hats in the ring instead.

In October 2020, it was eventually sold to a consortium of UAE-based businessman Murari Lal Jalan and Cayman Islands-based Kalrock Capital Partners despite Jalan’s links to the infamous Gupta brothers of South Africa. Adding to the puzzlement, the Consortium bagged Jet despite offering banks, employees and operational creditors – who had pegged their dues from the airline at Rs 24,888 crore – all of Rs 475 crore.

That is just the start.

Two years have passed since the Consortium bagged Jet Airways. This period has been one of stasis, with banks, employee associations and the new management locked in court battles. Last November, citing financial pressure, the consortium reduced pay for a third of its employees and put a smaller percentage on leave without pay. In this period, Jet 2.0 has also lost key executives and missed multiple deadlines to resume operations (see this, this, this and this).

As this article gets written, matters stay intriguingly poised. On one hand, NCLT has given the consortium six months to pay banks – but directed banks to transfer ownership in the meantime. Bankers are mulling an appeal. In the meantime, worried about unpaid gratuity, an employee association has gotten four Jet Airways Boeings impounded.

'In the meantime, worried about unpaid gratuity, an employee association has gotten four Jet Airways Boeings impounded.' Photo: Bill Wilt/Flickr (CC BY-ND 2.0)

This disarray needs to be understood. Its causal factors extend beyond the blame game underway between Jet’s ex-employees, banks and the Jalan-Kalrock Consortium. Take a closer look at its bankruptcy saga and you will see several of the deficiencies that haunt India’s Insolvency and Bankruptcy Code.

Apart from producing low loan recoveries for banks, it is also resulting in consequential – but little-discussed – changes in ownership over India’s private sector.

An airline pushed into bankruptcy

Why did Jet, India’s leading airline for so long, suddenly tip over into bankruptcy?

“Jet ran for 25 years,” a Mumbai-based investment banker had mused to this reporter in 2020. “It managed when crude was at $ 140 but fell when crude was at 48,” he said on the condition of anonymity.

Not just that, he added, the airline slipped into losses at a time when traffic was rising, competition was falling – rival airlines like Kingfisher, Air Sahara and Air Deccan had shuttered – and the number of domestic flyers was growing at almost 20%.

Here is what we know. The airline was debt-strapped, especially after it embarked on an aggressive expansion and acquired Air Sahara. Jet was also, as a former employee in Jet’s corporate communications team told this reporter in 2021, a high-cost operation. “Jet was a more inefficient setup than Indigo,” he said on the condition of anonymity. “Indigo had no aircraft on their books – they followed the sale and leaseback model. They also bought only one kind of plane and used it for everything. Jet, in contrast, had widebody, narrow and turboprops. It had Boeings and Airbuses. It had the highest cost/kilometres numbers in the business.”

Representative image. Photo: Vivek Prakash

The airline won a reprieve in 2013. Under CEO James Hogan, Etihad was investing in regional airlines like Virgin Atlantic, Air Serbia and AlItalia, trying to create a giant that could compete with rivals like British Airways and Lufthansa. That year, Jet founder Naresh Goyal sold a 24% stake to the Abu Dhabi airline which brought in money but demanded (and got) key positions like finance and network management. “Goyal didn’t like it but he didn’t have much choice,” said the ex-employee.

The deal stabilised Jet for a while. “And then, each of these airlines slipped into some trouble or the other,” said the ex-employee. “Etihad got busy fighting those fires, Jet, in contrast, was doing better and so, Goyal began turning the screws on Etihad.” The partnership went sour.

Then followed some bad quarters – a weak rupee plus high crude costs – which took a bigger toll on Jet than on its lower-cost rivals. Either way, unable to pay for its leased aircrafts, Jet slashed flights. This, however, reduced the airline’s income even as debt payments remained the same. By March 2019, 65% of its fleet had been grounded. The cash crunch worsened. Jet stopped flying in April that year.

Fresh working capital loans – paired with strict conditionalities for the management – might have saved the airline at this point. Those didn’t materialise. Jet’s senior management tried to attract fresh investors. Jet CFO Amit Agrawal, for instance, approached Tata Sons. Those talks went nowhere as well.

And so, in June 2019, Jet entered bankruptcy courts with creditors saying the airline owed them Rs 24,888 crore. What the airline needed at this time was a quick resolution. With its staff, slots, routes and aircrafts, it was still very much a going concern.

“The company should have been liquidated in a month,” a former president of the Confederation of Indian Industry told The Wire, on the condition of anonymity. “Look at how Satyam was handled.”

Also read: SEBI Has Been Repeatedly Embarrassed by Overturned Orders in Major Scams

What happened was very different. The airline saw a protracted resolution process – with the resolution professional needing to issue no less than three calls for buyers.

A resolution process with unknown bidders

Once the company was taken over by banks, the resolution process started.

In the first round, a clutch of familiar names evinced interest. Etihad was one. San Francisco-based private equity investment firm TPG Capital was another. Also in the running were Atlanta-based Delta Airlines, India’s National Investment and Infrastructure Fund and the Hindujas. None of them, however, submitted a formal resolution plan.

In the second round, in December 2019, a bunch of lesser-known entities stepped in. Apart from mining baron Anil Agarwal's family trust-backed Volcan Investments, two Russian funds (Treasury RA Creator and Far East Development Fund), an asset management company from Panama called Anantulo, Prudent ARC from Delhi’s Pitampura, and South America’s Synergy Group which holds a majority stake in Colombian carrier Avianca Holdings showed interest. Of these, only Synergy belonged to the aviation sector.

It was another reminder that India’s bankruptcy proceedings were drawing interest from unknown entities.

Take Treasury RA Creator. The Wire contacted a London-based academic studying Putin’s Russia, and she hadn’t heard of it. Another source sent a Russian article about the fund and its chairman Alexander Paramonov. The fund claimed to have 864.3 billion rubles (enough to put it on par with Russian bank Sberbank and oil-and-gas major Gazprom) but the figure seemed unlikely to be true, said the report. The fund is represented in India by one Binay Kumar. The Wire wrote to him, at the address on the fund’s website, but the email bounced.

As things stood, the second round fizzled out as well. None of the bidders submitted resolution plans. Then came the third round. Participants this time included Murari Lal Jalan and Kalrock Capital Partners; a consortium of Imperial Capital Investments LLC (a fund operating out of UAE), Flight Simulation Technique Centre Private Limited (FSTCPL), and Big Charter Private Limited; and Alpha Airways.

This round too was dominated by unknown entities. Jalan-Kalrock were unfamiliar names in the aviation sector. Imperial is an UAE-based fund with no information about its clients on its website. FSTCPL and Big Charter would make headlines in 2022 – after their abortive bid for Pawan Hans with another UAE-based fund.

Of these, only Jalan-Kalrock and Imperial submitted resolution plans. In June 2021, two years after Jet has stumbled into bankruptcy courts, Jalan-Kalrock was chosen.

The news took aviation sector experts – and those tracking Jet’s insolvency bid – by surprise.

Who is Murari Lal Jalan?

In both India and UAE, Jalan was little known before the acquisition.

“He is in real estate, with no background in anything who suddenly came up with a Rs 1,000 crore cheque,” the advisor to Jet Airways had told The Wire in 2021.

In the weeks and months that followed, however, worrying details emerged about Jalan. He had personal and professional relations with the infamous Gupta brothers (Ajay, Atul and Rajesh) of South Africa. Shashank Singhal, son of Atul Gupta, is married to Jalan's niece Shivangi – theirs was the double wedding attended by political bigwigs like then-CM and BJP leader Trivendra Singh Rawat, not to mention state BJP chief Ajay Bhatt and Patanjali’s Ramdev, that left the hill-town of Auli contemplating 24,000 kilos of garbage.

Also read: Finance Firm Buying Public Sector Central Electronics Ltd. for Cheap Has Links to BJP Leaders

In March 2021, Jalan acknowledged personal ties but denied any business links with the brothers. “Regarding the Gupta family, some of them are very good friends, but those are personal relations,” he told Rediff.com. “Professionally, I am not connected with them and I have no financial dealings with them.”

Two days after this article was published, The Wire received a response from the consortium repeating what Jalan had told Rediff.

“Mr Jalan continues to maintain that he has extended family relations with [the] Gupta brothers and has no business, financial or professional relationship with any of them,” it said. “Mr Jalan’s brother has family association with Gupta brothers and the family relationship of Mr Jalan’s brother and his family has no relation to the business activities of Mr Jalan. Each of them are separate entities, with their business activities, separate and distinct (sic).”

According to South African reporters, however, Jalan is working with relatives of the Gupta clan in at least two projects in Uzbekistan. The first is Minerva World of Knowledge, an international university being set up by Jalan’s MJ Developers.

Jalan at Minerva World of Knowledge. According to an Uzbek news website UZ Daily report, Jalan heads the project.

According to South Africa’s News24, Jalan is developing the university as a 50:50 partnership with Aakash Garg, who is married to Vega Gupta. Vega Gupta is the daughter of former Uttarakhand state minister Anil Kumar Gupta and Achla Gupta, the Gupta brothers’ sister.

The Wire had asked Jalan about these assertions. In its response, the consortium denied Garg held any equity. “Mr Jalan is the 100% legal and beneficial owner of MJ Developers, which is developing all the real estate projects in Uzbekistan including Minerva World of Knowledge; and Namangan Square and no other person (including Gupta brothers) have any right, interest, entitlement or ownership in any of Mr Jalan’s businesses,” it said.

Garg’s name, however, shows up on the website of Namamgan Square, a commercial-and-residential real estate project being developed in Uzbekistan by MJ Developers, where he is described as a core contributor. In addition, News24 had published two documents from 2019 – one containing registration details of Minerva World of Knowledge which suggests he held equal shares in the project; the other has been written by Garg to the Uzbekistan Prime Minister where he describes himself as a shareholder in the project. The Wire has asked the consortium to clarify.

Garg’s name also shows up on the website of Namamgan Square, a commercial-and-residential real estate project being developed in Uzbekistan by MJ Developers.

In addition, Amabhungane, an investigative journalism organisation focusing on political corruption in South Africa and neighbouring countries, flagged the joint participation of Jalan and the Guptas in a firm called Patanjali India Distribution.

In its response, the consortium accepted Jalan’s position at the firm but said he had left before the business got off the ground. “With respect to Patanjali India Distribution (an entity not associated or related to Patanjali Group), Mr Jalan was a non-executive director in Patanjali India Distribution Ltd, incorporated in 2019,” it said. “Until 2021, the company had no business or operations as it was never capitalized, and its bank accounts never opened and eventually in Dec 2020/Jan 2021, Mr. Jalan exited the company before it could commence any business.”

Apart from these, Zee News has reported about other business links between Jalan and the Gupta clan.

Notwithstanding Jalan's denials, these links have resulted in South African reporters – not to mention Indian newsrooms like Zee and Sunday Guardian – wondering if the Gupta brothers are backing Jalan.

As things stand, there is evidence that the brothers were interested in picking up firms through India’s bankruptcy auctions. In 2018, a company called Worlds Window Impex bid for Avantha Power’s thermal power project in Chhattisgarh. Worlds Window, as News24 found, was working for the Guptas.

That is not all. The Guptas have also been accused of putting pressure on South African Airlines to drop its Mumbai route so that Jet Airways could take over.

For this reason, it is also speculated that Jet founder Naresh Goyal, once seen as a front himself, was backing Jalan and Kalrock. “Goyal was pulling strings all over the place,” said the former advisor to Jet. “He propped up Jalan and Kalrock.” Narayan Hariharan, a former vice president at the airline, too felt Goyal was involved.

The Wire posed these questions to Jalan. Questions were emailed to both Jet 2.0 and Orion TechCity, a real estate business owned by him.

In its response, the consortium denied any links with Goyal. “It is from media reports that the Consortium came to know for the first time that any sought (sic) of alleged lobbying was done by Gupta Family for Jet Airways,” it said.

“With respect to Mr Naresh Goyal... Jalan/Kalrock/Florian Fritsch neither have nor ever had any business or personal relationship with Naresh Goyal or his family members. In fact, Mr Jalan and Mr Fritsch/ Kalrock do not know Mr Naresh Goyal, personally or professionally, and have never met him or interacted with him/his family till date,” it said.

And who is Kalrock Capital Partners?

As for Kalrock Capital Partners, registered in the Cayman Islands, it’s a cypher.

“Kalrock has no antecedents,” the advisor to Jet told The Wire in 2021. “No one has heard of them. They have not done any deals, they have not invested anywhere. They just have a website.”

According to an affidavit filed by Jet’s resolution professional, Ashish Chhawchharia, in the NCLT court, it’s an investment holding company for tech entrepreneur and investor Florian Fritsch. It will, says the affidavit, incorporate a wholly-owned subsidiary in the UAE.

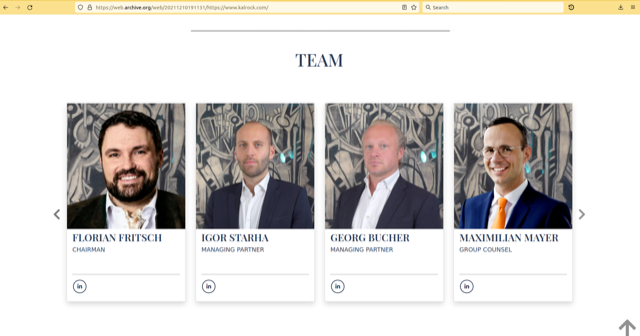

Now, Kalrock Capital’s website is www.kalrock.com. Till the middle of 2002, it disclosed the names of its management team – and the firm’s address. It doesn’t any more. As Wayback Machine shows, these details were removed sometime after 6 May, 2002.

Going by the website, Kalrock looks like a small firm with a few employees. Till 6 May, 2002, it only mentioned Florian Fritsch (chairman), Igor Starha (managing partner), Georg Bucher (managing partner), Maximilian Mayer (Group Counsel), Moritz Von Cramm (associate director) and Nils Stuben (associate director).

Going by Wayback Machine, Kalrock’s address is: 32 St George Street, W1S 2EA, London, United Kingdom.

Search for this address in the UK’s registry of companies and you will find Kalrock Capital Management. Its key people match those mentioned on the cache of the Kalrock website – Florian Fritsch and Igor Starha. Search the registry for Kalrock’s current address and the names of six companies show up – Starha Enterprises; Kalrock Capital Management; Kalrock Real Estate LLP; KRE Capital Ltd; MightyMo Ltd; and Relton Technologies.

These firms are related to each other, sharing not just the address but also key officers. In two cases, they also hold stakes in fellow companies. Starha controls Starha Enterprises. Fritsch and Starha control Kalrock Capital. Kalrock Capital controls Kalrock Real Estate. Starha Enterprises and Difumo Ltd control KRE Capital; Moritz Von Cramm controls MightyMo; and Stuben controls Relton. As for Difumo, it’s controlled by Georg Bucher.

These companies are very small in size. Take Kalrock Capital Management (KCM), one of Kalrock Capital Partners’ sister companies in London. It’s so small it doesn’t need to submit audited financial statements. It has just one employee. Its sister firms in London are no different.

There are two possibilities here. One, KCM could be a special purpose vehicle (SPV). “Financial institutions create an SPV (special purpose vehicle) and capitalise it when they have to pick up the shares,” said a Bengaluru-based venture capitalist, on the condition of anonymity. Two, on its archived website, Kalrock says it offers solutions for “special situations” where it “can be active partners and take board seats to ensure delivery of the business goals.”

And so, The Wire asked Chhachharia, Kalrock and Jalan what the two partners bring respectively to the consortium.

In its response, the consortium said both Jalan and Kalrock have “expertise in reviving and turnaround (sic) businesses”. The Wire has written back asking for instances where the two partners steered firms back to profitability. This article will be updated when it responds.

The consortium also said its stakeholders have received a security clearance from the Home Ministry and the Ministry of Civil Aviation after “a long and stringent background check and thus doubting their credibility and credentials would in effect mean doubting the Government of India including their investigation agencies involved in the entire process.”

We also asked Fritsch and Chhawchharia if Kalrock Capital Partners is big enough to invest in Jet Airways on its own – or if it would need capital at the time of investment.

If the latter, given its location in the Cayman Islands, what safeguards have the committee of creditors laid down to ensure Fritsch plows his own capital into Kalrock Capital Partners? This article will be updated when they respond.

In the meantime, poorly-known promoters are not the only reason the Jet transaction feels suboptimal.

There is also the matter of recoveries.

The other big downside

In the case of Worlds Window, the deal fell through. The firm could not arrange the money.

In the case of Jet too, disagreements over fresh claims and deliverables have resulted in court battles between banks, Jet employees and the consortium, with employees seeking their dues and banks and the consortium accusing each other of not delivering on commitments.

According to banks and employees, the consortium hasn’t made critical payments – to employees, lenders, towards capex and working capital – nor procured slots or international routes. As for the Consortium, it has accused banks of 'purposely delaying’ the implementation of the Jet revival plan and refused to take on additional claims imposed by an NCLAT order which told Jalan Kalrock to clear gratuity and provident fund dues of Jet Airways’ workmen.

These disputes need to be understood. Jet went into bankruptcy with total claims of Rs 24,888 crore. Of this, banks were owed Rs 8,000 crore. Against that, Jalan-Kalrock promised Jet’s stakeholders – employees, operational creditors and banks – Rs 475 crore. Banks were to get Rs 380 crore; employees, Rs 52 crore; and operational creditors, the remaining Rs 43 crore.

The remaining Rs 900 crore was for capex and working capital.

These are extraordinary numbers. At Rs 380 crore, banks recover just 4.7% of their dues. At Rs 52 crore, Jet employees get just a fifth of their statutory dues. When the NCLAT order came, the consortium wanted to accommodate the Rs 250 crore charge within this Rs 475 crore number – which meant recoveries by banks and operational creditors would fall further.

Needless to say, banks opposed this proposal. Instead, both banks and employees began wondering if Jet should be liquidated and not sold. The airline has about 12 aircrafts in its hangers. The value of its assets is estimated by sector watchers at Rs 2,000 crore.

This is dysfunction again. As Vinayak Chatterjee, the founder of infrastructure consultancy Feedback Infra, had told this reporter in 2018, “NCLT is essentially a banker’s solution to what is a larger problem.” In the case of Jet, banks and the consortium agreed to slash employees’ dues by 80%. The costs are coming home now. Both have been saddled with litigation.

In its response, the Consortium disputed these numbers saying: “As per the approved resolution plan, the monetary value of the revival package approved for Jet Airways lenders’ is more than Rs. 4,700 Crores and an additional upside on sale of aircrafts of Jet Airways and not mere INR 475 Crores as widely reported in news and media.”

However, according to Chhawchharia’s affidavit, uploaded on the Jet Airways website, payment for creditors stands at Rs 475 crore. “Rs 475 crores shall be used for payment to stakeholders from SRA's cash infusion,” it says on page 9. And so, The Wire asked the Consortium for more details.

As things stand, however, even Rs 4,700 crore works out to an 18% recovery of loans.

As this article was being finalised, the Supreme Court shot down the Consortium’s plea against the NCLAT order, directing it to pay the full Rs 250 crore. The Wire asked the Consortium if Jet will now fly. It said:

"The orders of the Hon’ble Supreme Court have no impact on the relaunch of Jet Airways. As a group carrying out business in India and as the new proposed promoters of Jet Airways, Jalan Kalrock Consortium is duty bound to comply with all applicable laws and non-appealable court orders and shall abide by all such orders.”

Questions

The deliverables from bankruptcy resolution are easy enough to define.

The stranded asset has to be revived. Losses to banks and other creditors should be minimised. Promoters shouldn’t covertly re-acquire their firms. At the same time, only capable firms should bag these assets – not political proxies round-tripping money into India; nor industry rivals trying to create monopolies or duopolies; nor global kleptocrats with access to zero-cost illicit funds.

In the case of Jet, India’s Insolvency and Bankruptcy Code has not delivered on these counts. The reasons run deeper than the factors specific to Jet – they lie in how the Bharatiya Janata Party-headed National Democratic Alliance has designed India’s bankruptcy process.

More on that in the concluding part of our report here.

M. Rajshekhar is an independent reporter studying corruption, oligarchy and the political economy of India’s environment. He is also the author of Despite the State: Why India Lets Its People Down and How They Cope.

Update: Two days after this report was published, the Jalan-Kalrock Consortium replied to the questions sent by The Wire to Murari Lal Jalan. The response is appended below.

How does the SC order on employee dues (upholding the NCLAT order) affect your plans for Jet’s relaunch?

The orders of the Hon’ble Supreme Court have no impact on the relaunch of Jet Airways. As a group carrying out business in India and as the new proposed promoters of Jet Airways, Jalan Kalrock Consortium is duty bound to comply with all applicable laws and non-appealable court orders and shall abide by all such orders.

I have a couple of questions about the Jalan Kalrock Consortium itself. It’s common in acquisitions for one party to bring in the cash and the other to bring in domain expertise. I wanted to understand the arrangement at Jalan-Kalrock. What do you and Florian Fritsch bring respectively to the Consortium?

The common belief you are referring to is aligned with the bidding process where technical and financial expertise of each member, relevant to the sector were looked at, for the purposes of any acquisition. However, in the case of Jet Airways, the committee of creditors were inclined in onboarding partners who had the expertise in reviving and turnaround businesses, which both Mr. Jalan and Kalrock have. The Jalan Kalrock Consortium was shortlisted by the lenders basis a stringent evaluation process conducted by them, and their advisors and it is not that Jalan Kalrock Consortium was self-qualified for the revival of Jet Airways. Jalan Kalrock Consortium has been shortlisted by the lenders of Jet Airways based on their merit and we remain committed for the revival of Jet Airways. In addition to this, the Ministry of Home Affairs, Government of India and the Ministry of Civil Aviation, Government of India have granted security clearance to each of Mr Jalan, Mr Fritsch, Kalrock Capital Partner Ltd, Cayman and each of the new proposed directors of the Consortium after carrying out a long and stringent background check and thus doubting their credibility and credentials would in effect mean doubting the Government of India including their investigation agencies involved in the entire process. The revival plan was submitted by Jalan Kalrock Consortium during COVID, when the aviation sector was one of the worst effected, with all aviation companies without exception suffering losses and no one inclined to enter the sector. Accordingly, the least Jalan Kalrock Consortium expects is some credibility for coming forward and taking the decision to revive Jet Airways. Jalan Kalrock Consortium is of the firm belief that revival of business is always better than liquidation and has full faith in the Indian Government, and the Indian legal and judicial system.

You have personal links with the Gupta brothers of South Africa. According to South African reporters, you are also partnering with the brothers on two projects in Uzbekistan -- Minerva World of Knowledge; and Namamgan Square. In addition, you have been a director on a firm owned by the Guptas called Patanjali India Distribution. Apart from these, Zee News has reported about other business links between you and the Gupta clan. In the past, however, you have accepted personal links but denied any professional relations with the Gupta brothers. Could you clarify this matter please?

Mr Jalan continues to maintain that he has extended family relations with Gupta brothers and has no business, financial or professional relationship with any of them. Mr Jalan’s brother has family association with Gupta brothers and the family relationship of Mr Jalan’s brother and his family has no relation to the business activities of Mr Jalan. Each of them are separate entities, with their business activities, separate and distinct. Mr Jalan is the 100% legal and beneficial owner of MJ Developers, which is developing all the real estate projects in Uzbekistan including Minerva World of Knowledge; and Namangan Square and no other person (including Gupta brothers) have any right, interest, entitlement or ownership in any of Mr Jalan’s businesses. With respect to Patanjali India Distribution (an entity not associated or related to Patanjali Group), Mr Jalan was a non-executive director in Patanjali India Distribution Ltd, incorporated in 2019. Until 2021, the company had no business or operations as it was never capitalized, and its bank accounts never opened and eventually in Dec 2020/ Jan 2021, Mr. Jalan exited the company before it could commence any business. Jalan Kalrock Consortium cannot control media reporting’s, or any statements made by any reporters or media houses. All these are mere allegations made by them without any documentary evidence or proof and made for reasons best known to them.

These links have resulted in persistent market speculation that the Gupta brothers are backing the consortium. Complicating matters, the Gupta brothers have lobbied for Jet Airways in the past (That was in SA), creating additional speculation that they might have been fronting for Naresh Goyal. Your comments, please.

As stated above, none of the consortium members have ever had any business association with Gupta brothers. It is from media reports that the Consortium came to know for the first time that any sought of alleged lobbying was done by Gupta Family for Jet Airways. With respect to Mr Naresh Goyal, he is not involved in Jet Airways in any capacity advisory, employment, investor, shareholder or otherwise. The consortium comprises of Mr Jalan and Mr Florian Fritsch of Kalrock Capital. Mr. Jalan/ Kalrock / Florian Fritsch neither have nor ever had any business or personal relationship with Naresh Goyal or his family members. In fact, Mr Jalan and Mr Fritsch/ Kalrock do not know Mr Naresh Goyal, personally or professionally, and have never met him or interacted with him/ his family till date. Accordingly, it is incorrect to state that Mr Naresh Goyal/ Gupta brothers are involved in Jet Airways and/or Gupta brothers are fronting Mr Naresh Goyal. The Consortium is undeterred by all such baseless rumours and are focused on their goal to put Jet Airways back in the skies. The Consortium has put together a strong and aggressive team, which is working round the clock to put everything together, so that the operations of Jet Airways can recommence at the earliest. In addition to this, it is put on record certain factual information regarding the total payout to lenders of Jet Airways by the Consortium under the approved resolution plan. As per the approved resolution plan, the monetary value of the revival package approved for Jet Airways lenders’ is more than Rs. 4,700 Crores and an additional upside on sale of aircrafts of Jet Airways and not mere INR 475 Crores as widely reported in news and media.

Note: This article was updated at 1:05 pm on February 25, 2023 after the Jalan-Kalrock Consortium responded to The Wire's questions.

This article went live on February twenty-third, two thousand twenty three, at thirty-five minutes past eight in the morning.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.