A Forward-Looking Survey Projects Decline in Private Capex

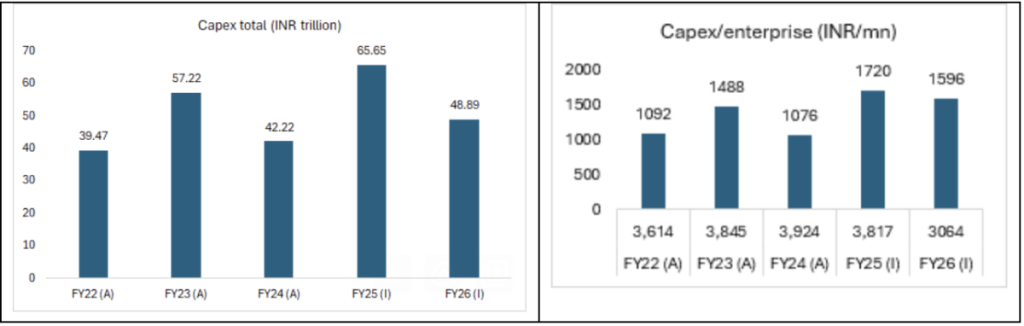

The inaugural forward-looking survey on private capex investment intentions by the Ministry of Statistics and Programme Implementation indicates a massive 25% year-over-year decline in intended private capex in FY26(I) to Rs 4.88 trillion, over Rs 6.56 trillion in FY25. For FY26 capex intent, the responding enterprises at 3064 are also 20% YoY lower. The actual capex for FY22 to FY24 shows a better growth of 9% CAGR at Rs 4.22 trillion. But that is a statistical bounce from the COVID-19 shock.

As per the MoSPI report, the decline in intended private capex reflects a conservative approach and apprehension of the reporting firms, which is likely to have been impacted by deteriorating demand conditions, cutback of government capex and concerns of global protectionism ahead of the change of guard in the US. The survey was conducted from November 2024 to January 2025.

The survey covered 16,025 large enterprises selected using sectoral sales thresholds, translating into a sample size of 5,380.

Of the lower sample of 3064 responding enterprises for FY26, only 71% or 2172 expressed capex intent. The average capex of Rs 1596 million and total capex intent of Rs 4.88 trillion in FY26 is only 5.5% CAGR over FY22 actual or approximately 1.5% in real terms, assuming average WPI inflation of 4%.

The other notable insights from the survey are that intended private capex is led by manufacturing with a 43.8% share (FY25), followed by Information and Communication (15.6%) and Transportation and Storage (14%). Over 53% of capex was allocated to machinery and equipment.

The survey notes that its findings do not reflect the complete private capex picture as a) it excluded small firms and certain special purpose vehicles with no turnover, b) cautious responses due to pending approvals, and c) issues relating to data entry and NIC core selection.

Forward-looking survey on Private CAPEX Investment Intentions by MoSPI

Source: MOSPI, Systematix Research, A=actual, I=intended, numbers in the second chart are the number of respondents in the survey.

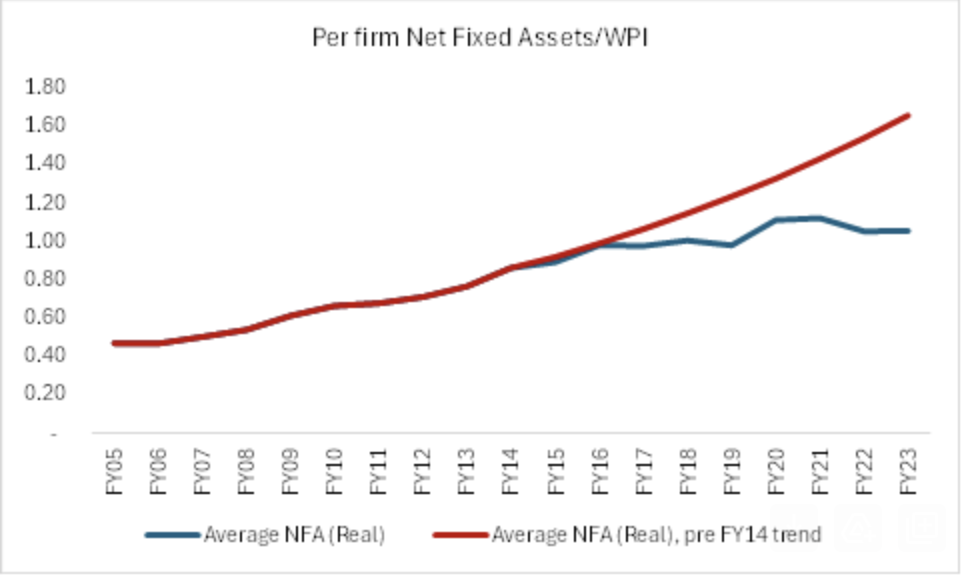

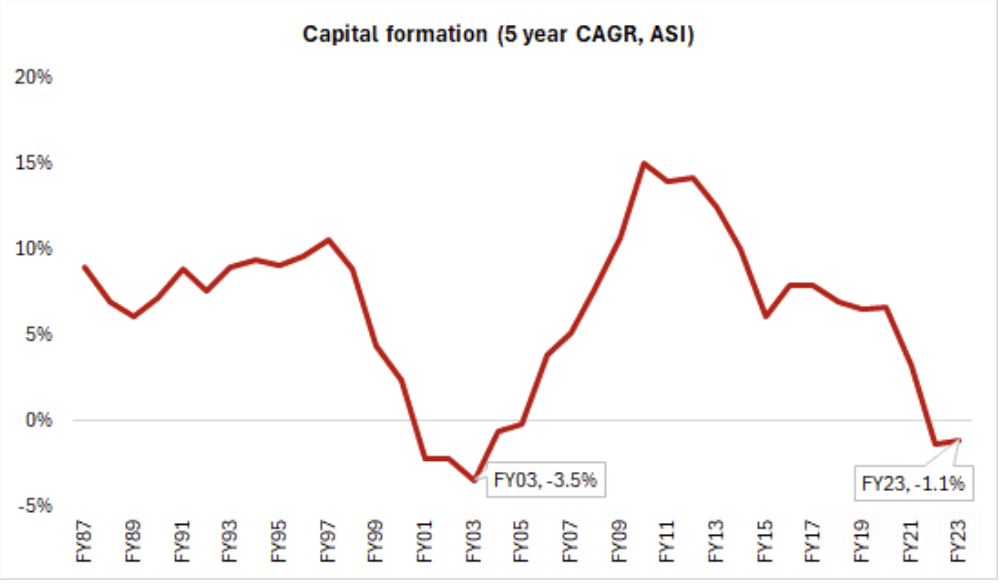

To broaden the perspective, we also assessed the compilation of private capex data from the CMIE and MOSPI’s long-term Annual Survey of Industries (ASI) available since FY74. We consider the nominal growth of net fixed assets of aggregates of domestic private companies (CMIE varying sample of 32,100 companies, FY23) and fixed capital of all industries from ASI (253 thousand firms). We derive capital formation by deflating by WPI.

For the CMIE sample, the average net fixed capital of INR 1.61 billion grew by 6.9% 5-year CAGR and 1.2% in real terms. On a 9-year real basis, since FY14, it averaged 2.3% compared to 7.6% in FY14.

Fixed capital of all industry estimated by ASI stood at INR 41.2 trillion and INR 162 million per firm and grew by a 5-year CAGR of 4.6% and 3.3%. And in real terms, the average fixed capital declined by 1.1% per annum, considerably lower than the average of 10% in FY14 and the peak of 15% in FY10.

Thus, the enervating capex intent of Indian private companies indicated by the latest MOSPI’s forward-looking survey mimics the data from CMIE's compilation. The counterfactual trend extrapolated from the average 5-year growth till FY14 would imply that the current level of net assets on the books of domestic companies is lower by a significant 36% (CMIE service). The ASI data captures a larger universe, and hence, the contraction in real fixed capital for its sample indicates a worse scenario for smaller firms.

CMIE: Aggregate net fixed assets of domestic private companies (real)

Source: CMIE, Systematix Research

ASI: Average fixed capital/factory (real)

Source: ASI-MOSPI, Systematix Research

From the outlook standpoint, with the uncertainty accentuating due to the US-led global tariff conflicts, the intended private capex may likely decline more than the 25% fall projected by the survey. The sharp deceleration in sales growth of non-finance companies in FY25 is accompanied by companies optimising operating costs and adopting automation to conserve profitability. Hence, private capex revival will continue to remain elusive. Following the rapid past 6-7 years, the scope for government capex is also receding, given the tightening fiscal constraints. Policy focus has shifted to regulatory and monetary easing by the RBI. It remains to be seen if this slender stimulus can be effective in reviving both consumption and investment demand simultaneously.

Over the past decade, we have not had a chance to change our verdict that private capex turnaround is still afar. Before the COVID-19 pandemic, it was a combination of domestic shocks, weak consumption demand, skewed supply-side policies and rising global protectionism that were responsible.

Looking ahead, the rising global fragmentation will be responsible; the decline in private capex as per the latest survey, amply demonstrates that the tariff war triggered by the US will have a much larger impact than the widely assumed insularity view on India.

Dhananjay Sinha is co-head of Equities and head of Research of Strategy and Economics at Systematix Group.

This article went live on May eighteenth, two thousand twenty five, at eight minutes past seven in the evening.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.