Growing Evidence of a Vanishing Middle Class, Struggling Low-Income Class in India

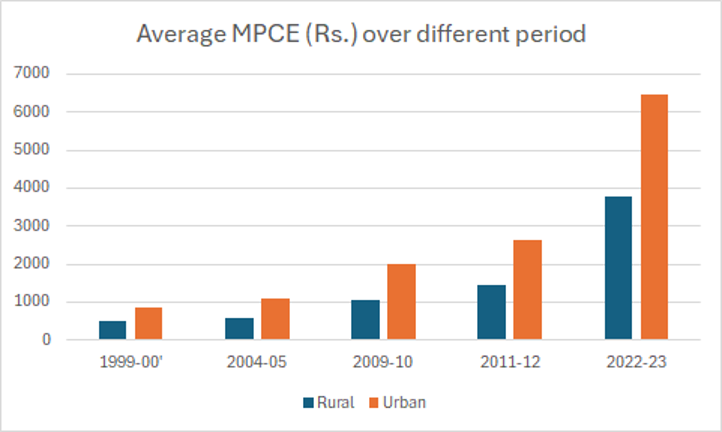

The Monthly Per Capita Consumer Expenditure (MPCE) data recently made available, from 1999-2000 to 2022-23, indicates a significant upward trend in the consumer expenditure levels of households across both rural and urban areas. This trend, in the period between 2012-13 and 2022-23, has observed the double whammy combined effects of sporadically rising inflation and stagnating real wages, which in the last decade provide evidence of a worsened per capita standard and quality of life for most Indians (if understood in terms of the economic and consumption choices made available to households).

See the chart below for reference:

Source: Author’s Calculations from NSSO Data

The period from 2009-10 to 2011-12 saw a remarkable surge in MPCE, suggesting a rapid increase in spending power amongst households possibly driven by robust economic growth. From 2011-12 to 2022-23, MPCE continued to rise steadily, but incomes in this period didn’t grow at the same pace for most income households. The widening gap between rural and urban MPCE levels over the years further highlights the ever deepening urban-rural economic gulf that has been explained (and exacerbated) by a K-shaped nature of economic growth trajectory, especially in the post-covid period.

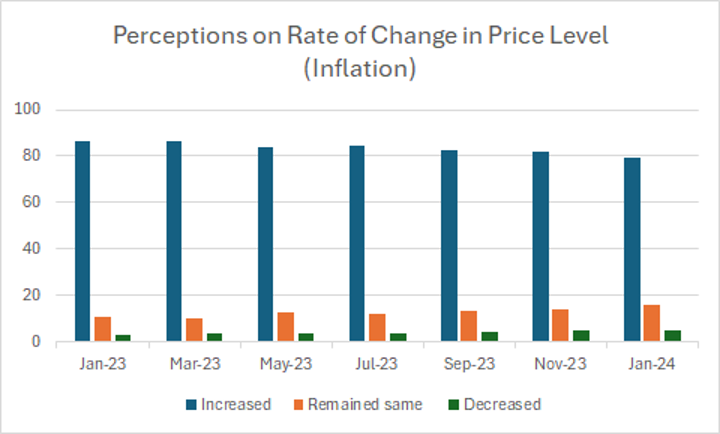

Source: Author’s Calculations from RBI consumer confidence survey

The data above illustrates a notable shift in perceptions regarding the rate of change in the price level (inflation) over the specified period from January 2023 to January 2024. There is a consistent decline in the proportion of individuals perceiving an increase in prices, decreasing from 86.5% in January 2023 to 79.5% in January 2024.

This decline suggests a diminishing concern or awareness of inflationary pressures among the population. The evolving perception of inflation has the potential to impact consumer confidence, spending patterns and overall economic activity. Decreasing perceptions of inflation may lead to increased consumer confidence and overall spending, contributing subsequently to economic growth-however that hasn’t really happened in the way perception amongst income groups has been measured.

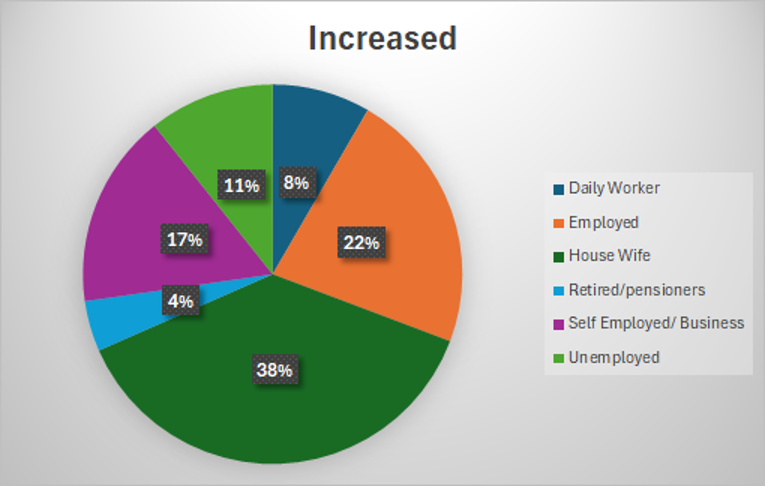

Source: Author’s Calculations from RBI consumer confidence survey

Expectation of higher prices amongst employed and self-employed categories, with 22% and 17% respectively, indicates a growing concern. This sentiment suggests potential challenges ahead, as rising prices can erode purchasing power, leading to reduced consumer spending. Such a scenario could dampen economic growth and exacerbate inflationary pressures, impacting overall economic stability. Addressing these concerns is crucial to maintaining consumer confidence, sustaining economic growth, and ensuring affordability for essential goods and services.

Below we discuss the findings of the RBI Consumer Survey data which provides a direct alignment with the household consumption data released recently.

Evidence for a K-shaped India

A closer look at the RBI’s Consumer Survey time-series data reveals glaring inequality staring at the face of India’s sluggish economic growth story. The K-shaped growth pattern becomes more evident when one carefully aligns the consumer confidence and perception data with other macroeconomic realities: real wages, consumption patterns, employment growth, household debt and a widening credit-GDP gap (creating excess liquidity concerns for the central bank).

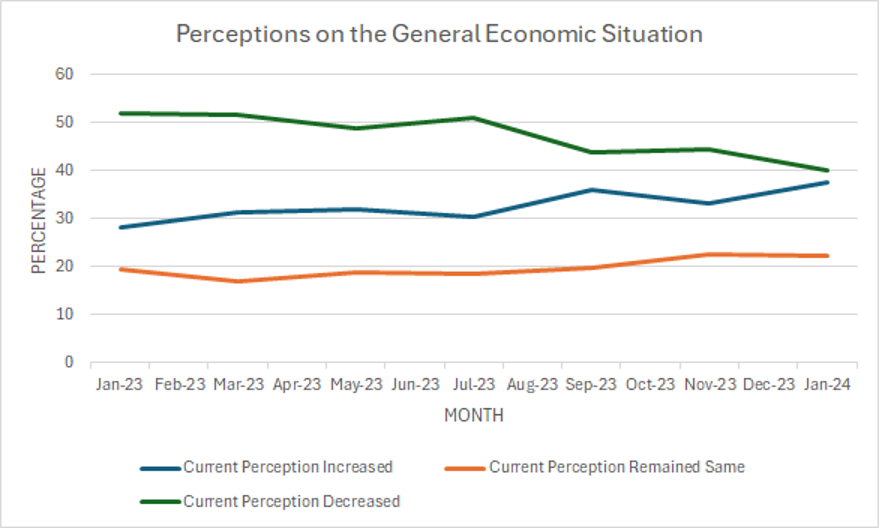

Source: Author’s Calculations from RBI Consumer Survey (February, 2024)

From January 2023 to November 2023, a downward trend in the perception of the general economic situation is evident amongst Indians (see here for a more detailed analysis). Over this period, the percentage of individuals perceiving a decrease in the general economic condition consistently exceeds those reporting an increase or maintaining the same perception.

This prolonged pattern suggests a prevailing atmosphere of pessimism or economic uncertainty, reflecting broader concerns of adverse public sentiments and dis-confidence in economic prospects amongst certain economic groups, which, as crisis economists explain, have their own multiplier effect (amplifying its effect on other aggregates) over time.

From the RBI data, in January 2024, a temporal shift in perception compared to previous months is also evident for some income brackets, with a notable increase in the percentage of people perceiving an improvement in the economic situation, rising from 33.1% to 37.5%. Conversely, the percentage of individuals perceiving a decrease in the economic situation has decreased, dropping from 44.4% to 40.2%.

The chart below shows quite clear evidence of what has been perceived as a K-shaped economic recovery for India over the last few years, in the post Covid period.

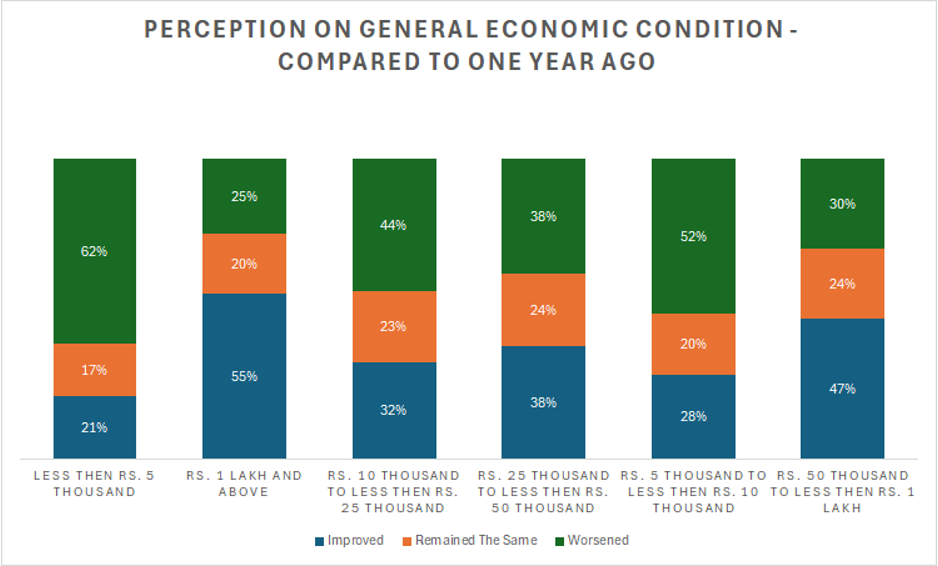

The perception of the general economic situation varies significantly across different income brackets, as revealed by the provided data.

For individuals earning less than Rs 5,000, a concerning trend emerges, with the majority (62%) perceiving a monthly worsening economic situation. In contrast, only 21% report an improvement. This persistent negative perception suggests ongoing financial strain or challenges within this income group.

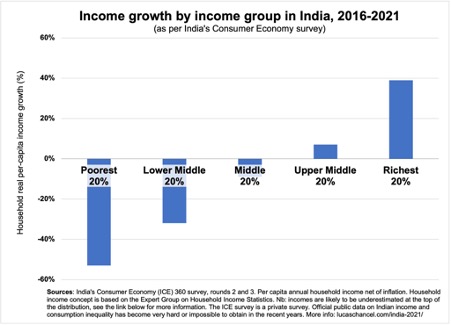

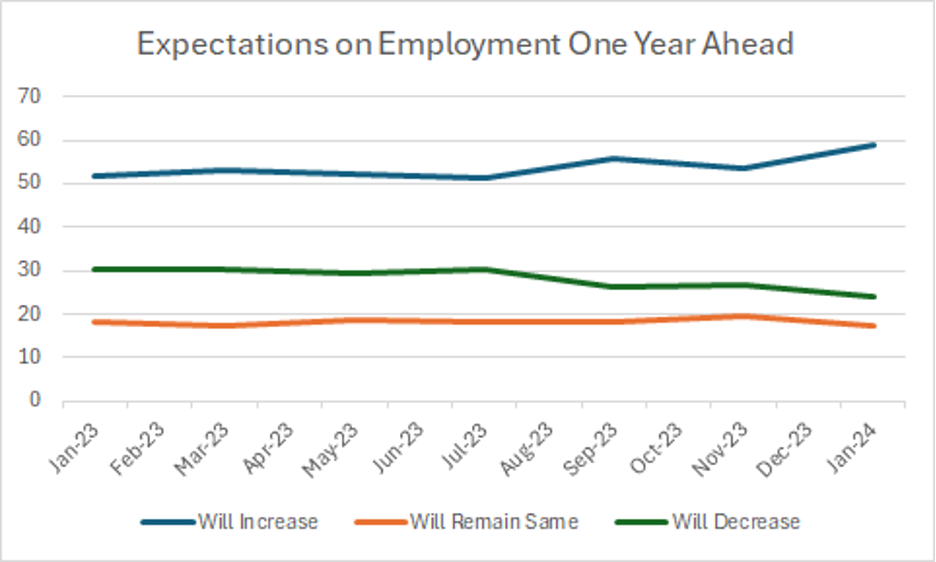

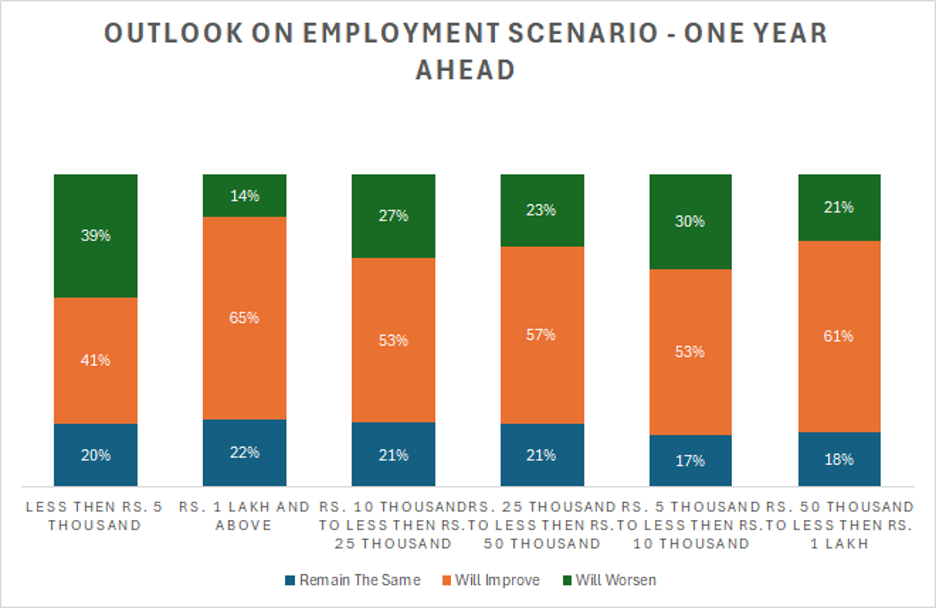

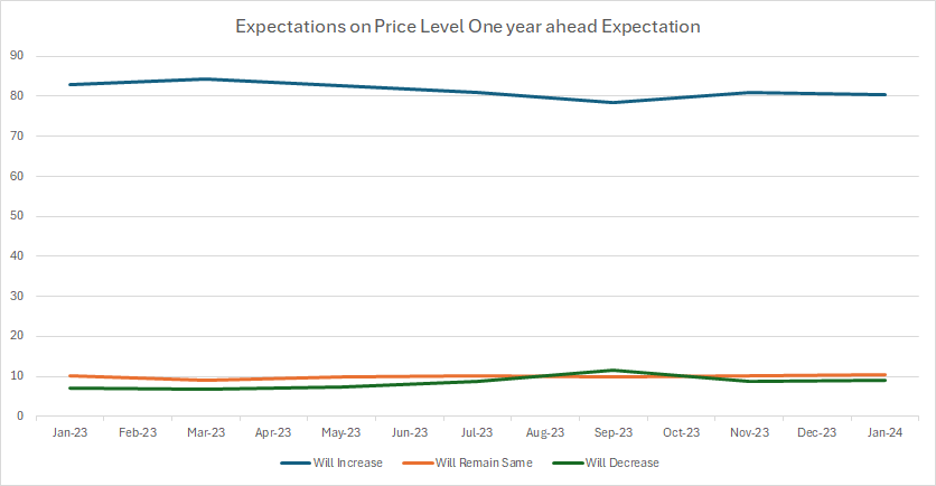

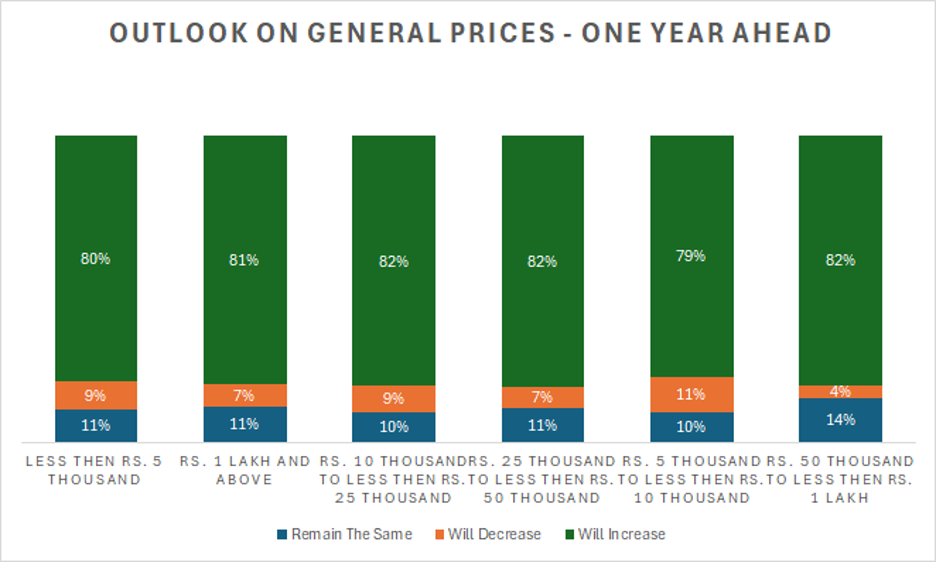

Similarly, for those earning between Rs 5,000 and Moving up the income scale to Rs 10,000- For individuals earning between Rs 50,000 and Finally, the highest income bracket of Rs 1 lakh and above demonstrates the most positive perception, with 55% reporting an improvement monthly. Only 25% of individuals in this group perceive a worsening economic situation, indicating a largely optimistic outlook among higher-income earners. See below for a macro-reality check on how real incomes have stagnated across income groups. Overall, the data underscores the significant impact of income levels on perceptions of the general economic situation, with lower-income groups expressing more negative sentiments compared to their higher-income counterparts. Expectations on employment one year ahead amongst Indian consumers Source: Author’s Calculations from RBI Consumer Survey (February, 2024) The percentage of respondents anticipating an increase in employment fluctuates slightly around the low 50s, while those expecting a decrease remain around 30%. This suggests a consistent level of optimism regarding future employment prospects throughout this period, with only minor variations. However, by September 2023, there's a noticeable uptick in the percentage of respondents predicting an increase in employment, reaching 55.8%. This indicates a growing confidence in future job opportunities among the surveyed individuals. Conversely, the percentage of those anticipating a decrease in employment drops to 26.2%, reflecting reduced pessimism or concern about future job prospects. This trend continues into January 2024, where the optimism regarding future employment prospects sees a significant boost. The percentage of respondents expecting an increase in employment rises to 58.7%, reaching its highest point in the provided data. Meanwhile, the percentage of those predicting a decrease in employment further decreases to 24%, indicating a substantial decrease in pessimism and a heightened level of confidence in future job opportunities. Source: Author’s Calculations from RBI Consumer Survey (February, 2024) For individuals earning less than Rs 5,000, there is a considerable divide in expectations. While 41% anticipate an improvement in employment, a significant portion (39%) expects worsening conditions, indicating a mixed sentiment within this income bracket. Conversely, respondents in the highest income bracket of Rs 1 lakh and above demonstrate the most optimistic outlook, with a substantial 65% expecting an improvement in employment. Only 14% of individuals in this group anticipate worsening conditions, reflecting a strong confidence in future job prospects among higher-income earners. Among those earning Rs 10,000- However, a notable proportion in these groups (27% and 23% respectively) still foresee worsening conditions, suggesting some degree of uncertainty or concern despite overall optimism. In the middle-income brackets of Rs 5,000-<10,000 and Rs 50,000-<1 lakh, expectations are also predominantly positive, with 53% and 61% respectively expecting an improvement in employment. However, a significant minority in these groups (30% and 21% respectively) anticipates worsening conditions, indicating some level of cautiousness or apprehension despite overall optimism. Overall, while there is a general trend of optimism across most income brackets regarding expectations on employment one year ahead, there are variations in the level of confidence and concerns, with higher-income groups demonstrating a stronger belief in positive outcomes compared to lower-income counterparts. Expectations on price level one year ahead Source: Author’s Calculations from RBI Consumer Survey (February, 2024) From January 2023 to November 2023, expectation among respondents for an increase in prices one year ahead seems to continuously be rising, with percentages increasing from 78.4% to 84.3%, suggesting a higher inflationary expectation amongst the surveyed individuals during this period. In July 2023, there's a slight decrease in the percentage of respondents expecting an increase in prices, dropping to 80.9%. This dip is accompanied by a corresponding increase in the percentage of those expecting prices to remain the same or decrease, indicating a temporary shift in sentiment regarding future price levels. However, this shift appears to be short-lived as the expectation for price increases rebounds in subsequent months. By January 2024, the percentage of respondents anticipating an increase in prices stands at 80.5% like the levels observed in earlier months. Overall, the trend in expectations on the price level one year ahead suggests a consistent anticipation of inflation or higher price levels among respondents, with occasional minor fluctuations in sentiment observed throughout the period. This reflects ongoing concerns or expectations regarding future economic conditions and their potential impact on prices. Source: Author’s Calculations from RBI Consumer Survey (February, 2024) Across all income brackets, most respondents expect prices to increase one year ahead, with percentages ranging from 79% to 82%. This suggests a widespread belief among surveyed individuals that inflation or higher price levels are likely in the coming year. Furthermore, the percentage of respondents expecting prices to remain the same or decrease is relatively low across all income brackets, ranging from 7% to 14%. This indicates a consensus among respondents that price stability or decreases are less likely compared to increases. Among different income groups, there are minimal differences in expectations regarding future price levels. Regardless of income level, respondents express similar sentiments regarding the likelihood of price increases, with only slight variations in the percentages expecting price stability or decreases. Overall, the trend in expectations on the price level one year ahead reflects a shared anticipation of inflation or higher price levels among respondents, irrespective of their income bracket. This suggests a broad-based perception of economic conditions and their potential impact on future prices. Deepanshu Mohan is Professor of Economics and Dean, Office of Interdisciplinary Studies and Director, Centre for New Economics Studies (CNES), O.P. Jindal Global University. Aryan Govindkrishnan is a Masters student at Jindal School of Government and Public Policy and a team co-lead for CNES’ InfoSphere team. The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.