'Household Savings Hit Record Low at 5.2%, Debt at All Time High in FY23': RBI

New Delhi: Household savings hit a record low at 5.2% of the gross national disposable income (GNDI) in FY22-23 while debt rose to an all-time high at 5.7%, the RBI annual report for 2024 shows. GNDI refers to the income available to the nation for final consumption and gross saving.

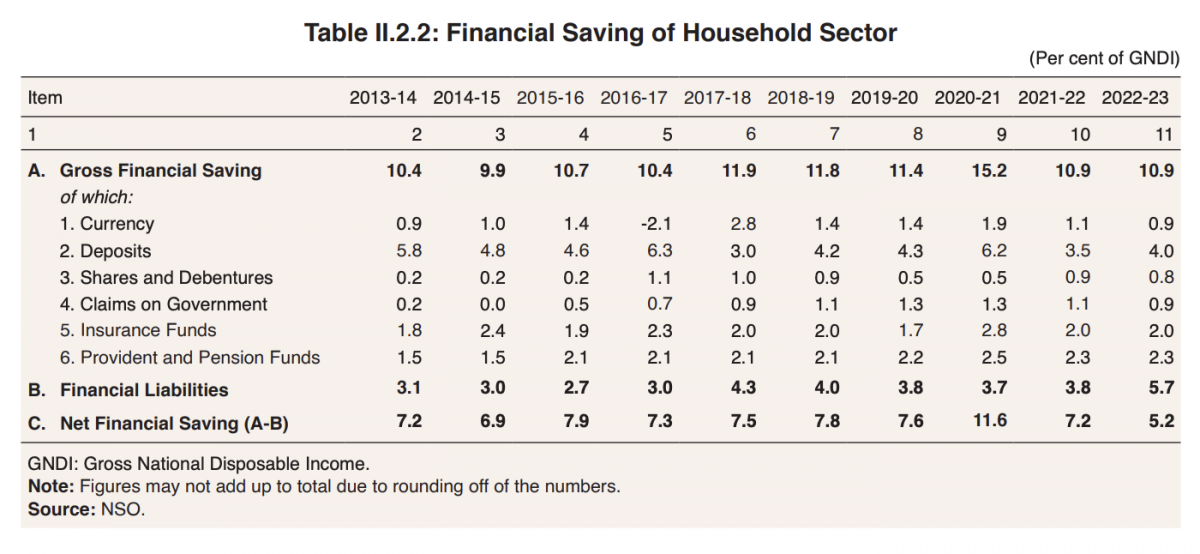

The report shows that net financial savings of households have stagnated over the last decade, hovering around 7.5%, except the pandemic year FY20-21 where savings peaked at 11.6%.

However, in FY21-22, savings saw a sharp drop to 7.2% before falling to an all-time low of 5.2% last year.

Gross financial savings also hovered around 10-11% over the past decade except the pandemic year FY20-21 where they peaked at 15.6%.

Lower gross savings means that people are saving less and consuming more, which, in turn, results in less domestic investment.

According to the RBI report, the savings-investment gap widened in FY22-23.

Screengrab from RBI report.

Meanwhile, household debt rose from 3% in FY13-14 to a record high of 5.7% in FY22-23.

Over the last decade, debt levels hovered around 3-4% except FY15-15 when it hit a low of 2.7%. Compared to FY21-22, when household debt was at 3.8%, the last fiscal year saw a massive jump in household liabilities to 5.7%.

High debt and low savings have come at a time when the country is seeing large scale unemployment and stagnant wages.

Unemployment and stagnant wages

According to the latest ILO report on India's labour landscape, the proportion of unemployed youth with an education has surged from 54.2% in 2000 to a staggering 65.7% in 2022, Business Insider reported.

For those with a college degree, the unemployment rate stands at 29.1%, nearly nine times higher than the unemployment rate for illiterate individuals (3.4%), the ILO report said.

Meanwhile, another ILO report prepared in collaboration with the Institute for Human Development (IHD) showed that the average monthly real earnings of regular salaried workers declined by 1% each year between 2012-22.

According to the ILO's calculations based on official government data, the average real monthly wage of a regular wage worker decreased from Rs 12,100 in 2012 to Rs 10,925 in 2022.

Regular wage or salaried workers are individuals who have relatively long-term employment and are paid on a weekly or monthly basis. This includes government employees, Accredited Social Health Activist (ASHA) workers, domestic helpers, guards, and those employed in the private sector.

The decline in wages was also observed among agricultural workers. From 2014-2024, real wages (wages that have been adjusted for inflation) for agricultural labourers declined by 1.3% every year according to data from the Ministry of Agriculture. The decade before that (2004-2014) was marked by an annual rise of 6.8% in real wages for this sector.

Those who work in brick kilns, seen as labour intensive and a last resort to gain employment for India’s poorest, too saw a stagnation of wages in the last decade.

This article went live on May thirty-first, two thousand twenty four, at thirty-two minutes past two in the afternoon.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.