What Does the Future of RBI's Inflation Targeting Look Like?

Every policy announcement made by the Indian government or the Central bank is closely monitored by both winners and losers.

One such defining institutional framework which has recently been debated extensively is the “Monetary Policy Framework Agreement” or the “Flexible Inflation Targeting (FIT)” framework.

Put simply, this was an arrangement that came about in early 2016, whereby a monetary policy committee within the RBI would target inflation – consumer price inflation – which was legally decided to be a wide band of 2%-6% with 4% as the mid-point.

The legal provision provides for a review of “this inflation target” after every 5 years.

The reason for the monetary policy framework catching headlines recently has been two fold – first, the tenure of the Monetary Policy Committee (MPC), which decides the policy interest rates in the country, came to an end at the end of its last meeting. Second, the inflation target is due for review in the next six months i.e March 2021.

On Monday night, after some puzzling delay, a new MPC was formed with the appointment of three new external members.

Deliberations on the latter will be an ongoing affair as the winners will harp on the benefit of low retail inflation during most of the past four years while losers will voice the growth concerns regarding the economy. The question of “Did the FIT pass the litmus test of its stated objective?” will provide important cues for the future course of action.

Did FIT achieve its stated objective?

The mandate explicitly states that the MPC has to ensure price stability while keeping in mind the objective of growth. During these past four years, the Indian economy has experienced a mix of low inflation, sticky inflation, high growth and low growth. The only positive is that the economy did not witness double digit inflation as was the case prior to 2014.

So prima facie, the framework looks to have ensured price stability. But can this benign inflation be completely ascribed to the framework? Has it come at the cost of slowdown in the economy? To understand this, we look at a few key variables which are restricted to inflation and growth to understand the efficacy of the FIT.

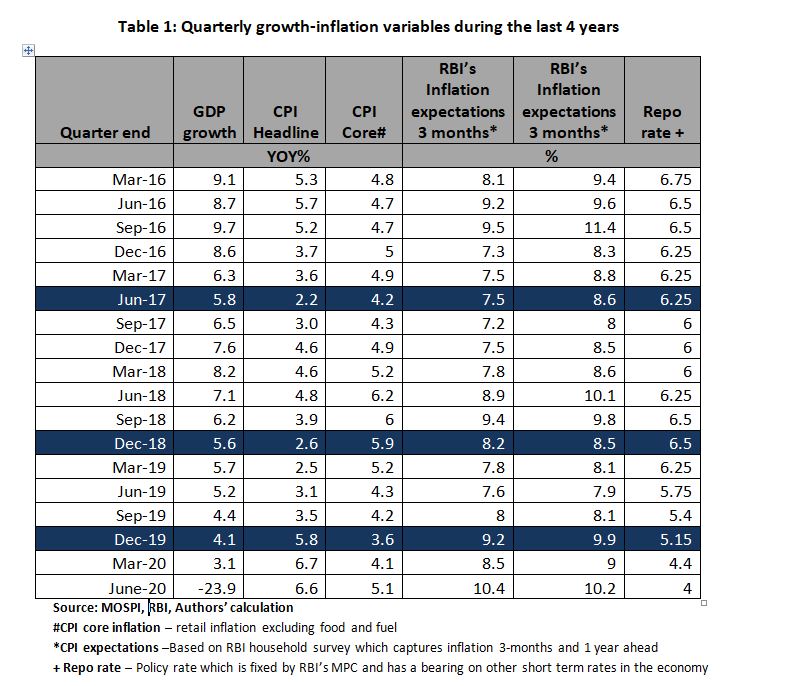

Two points which are clearly evident from the table below is that monetary policy has broadly been easing i.e reduction in policy repo rate, barring two periods of tightening i.e increase in repo rate. Despite policy rates cuts, inflation has largely remained benign and within target almost throughout this period barring Q4-FY20 and the COVID-19 period. Therefore, moderate inflation either due to slightly tighter policy or certain structural reforms on the supply side can be conjectured but cannot be pinpointed. Second, contrary to policy outcomes, economic growth has fallen from a peak of 9.7% to as low as 3.1% in March 2020.

Three phases (highlighted in Table 1) stand out, emphasizing the discretion in a rule based environment.

Two of these three phases i.e. June 2017 and December 2018 was when despite growth moderating and inflation (including expectations) easing, policy repo rates remained unchanged. The third phase (December 2019), the RBI cut the repo rate by 35 bps in spite of inflation being closer to the 6% mark and inflation expectation rising. The discretion is alright but could have been more consistent across the tenure. Overall, neither benign inflation nor muted growth can be completely ascribed to a tight monetary policy but efficacy of the FIT to tame inflation cannot be totally undermined.

Proposals for the next 5 years

A host of proposals by eminent economists have been put forth on the discussion table with some voicing their opinion to abandon the framework while others expressing tweaks. It is important to know that the law only talks about review of the inflation target and not the framework. Nonetheless, let’s look at the various propositions in the platter. First, V. Anantha Nageswaran, member of the Economic Advisory Council argues in abandoning the inflation targeting framework as it is ill-suited for central banks in both developed and developing countries for idiosyncratic reasons. He gives examples of advanced economies in failing to raise the inflation rate since the global financial crisis (GFC) of 2008, while pointing out supply-side rigidities in developing economies which makes the framework toothless. He suggests a need to move back to “multiple indicator approach” followed between 2008 and 2013 or target a variable like credit growth, which the RBI can control.

Second, Sabyasachi Kar augments the flexible inflation targeting regime with an unconventional monetary fiscal coordination. To put it simply, he suggests a dimension of direct monetisation of the “government capital expenditure” by the RBI keeping inflation within targets.

Third and as required by the law, there have been voices to revise the inflation target. Here, the discussion has broadly revolved around – increasing the inflation tolerance limit and whether core inflation should be the target. The most likely change could be seen in revising the inflation target higher but economic commentator Niranjan Rajadhyakasha points out that this should be empirically grounded and not delinked from the overall global inflation trend. The argument on changing the anchor to core inflation emanates from the volatility in food and fuel prices. This is a valid consideration but research showing mixed results of second round effects of headline retail inflation on core inflation will have to be closely scrutinized. Last, the revision in the measurement of the retail inflation index based on a new consumption survey will sooner or later add to the debate.

An increase in the inflation target band will indirectly rope in the secondary objective of growth into the monetary policy equation while a suggestive band for core inflation or household inflation expectations could further minimize the discretion in the policy decision. In spite of the instances of discretion in monetary policy stated above and the post-COVID-19 supply-side induced inflationary concerns, the flexible inflation targeting regime should continue with some minor tweaks for the next 5 years as well.

Sushant Hede is an Associate Economist at CARE Ratings Views expressed are personal.

This article went live on October sixth, two thousand twenty, at fifteen minutes past two in the afternoon.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.