Will the Modi Govt Fix the Economy With the Union Budget 2025?

This is the first part of a series of macro-analyses by the InfoSphere team of the Centre for New Economics Studies (CNES).

As various stakeholders gear up for the Union Budget 2025–26 , the atmosphere is charged with uncertainty, considering recent economic headwinds and the economy’s troubling growth trajectory.

Despite the optimism that accompanied the beginning of the fiscal year, growth unexpectedly slowed in the second quarter to 5.4%, with the economy grappling with a slew of challenges – sluggish capital formation, weakening consumer demand and the ripple effects of adverse weather conditions. These factors have cast a shadow over the otherwise resilient trajectory that India has been on – making this budget a critical moment for steering the economy back on track.

This year’s budget is widely expected to take a more aggressive stance on attracting both foreign and domestic investments to improve public health infrastructure among other critical sectors. In ten years of the Modi government, this aggressive posturing, banking on capex-fueled government spending, hasn’t worked.

One may expect a slew of new factor market reforms and/or state-designed incentives designed to position India as a magnet for private capital, while also encouraging homegrown enterprises to expand.

Low consumption demand, stagnant real wages

Such measures are seen as essential for reviving the economic momentum and sustaining long-term growth. However, low urban consumption demand, weak growth in real wages across sectors and a constant state of high unemployment has translated into poor performative metrics for domestic private capital expansion.

It is hoped that this year’s Union Budget offers more substantive support for the MSME sector and industrial clusters that form the backbone of India’s manufacturing and service industries and the labor-intensive employment it offers. The pandemic’s scars and recent economic tremors mean that targeted incentives and reforms in this space could prove pivotal for job creation and broader economic stability.

Additionally, with the middle classes being squeezed from taxes (from both direct and indirect), long-awaited tax breaks are essential for boosting disposable incomes and reigniting consumer confidence, especially in urban areas where consumption demand is weak. With household budgets stretched thin, the common citizen is eagerly awaiting policy measures that can ease financial strain and fuel spending.

Also read: The Indian Economy Is Being ‘Destabilised’ by Cronyism, Not Hindenburg or Soros

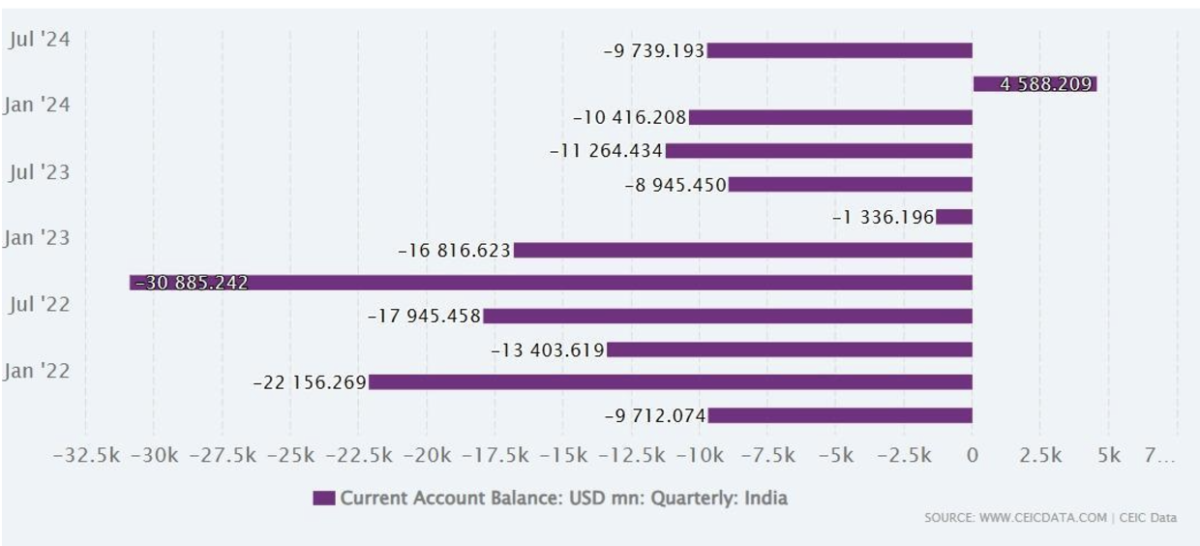

In the fiscal landscape, Q3 saw dwindling net exports, with the current account deficit widening to 2.8% of GDP – a disappointing deviation from the projected 2%. Sluggish growth was most apparent in manufacturing, while mining reported net negative growth.

At the same time, consumer demand has remained fragile. Reports from Nomura underline growing household balance sheet stress, with rising income disparities and limited savings deepening India’s cyclical slowdown. While urban demand shows some signs of recovery, rural consumption continues to face significant strain due to inflationary pressures and erratic monsoons. Reinvigorating consumer confidence through measures such as tax breaks or direct support could be key to addressing these economic hurdles.

Source- CEIC Data

The problem of GST

Since its implementation, GST collection has not met the promised growth. The average monthly growth rate from April 2022 to October 2024 was only 0.86%. This marks a contrast with the promised 14% annual growth in state revenue with the introduction of GST.

With the end of the compensation mechanism in 2022, many states face significant fiscal constraints which have increased their financial difficulties. The state also had to cede approximately 44% of their taxation rights with the imposition of GST, resulting in a reduction in fiscal autonomy for states over their tax policies. It has also reduced the flexibility that states enjoyed in the pre-GST era, when they were able to adjust tax rates according to their states’ economic conditions.

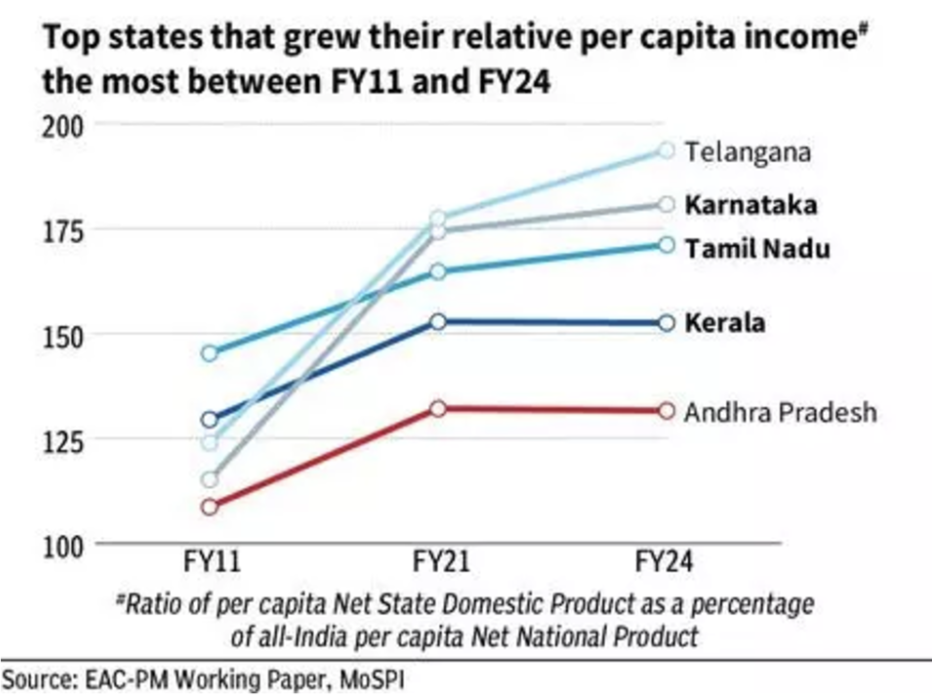

Source: EAC-PM working paper, MoSPI

A report by the National Stock Exchange highlights a critical revenue disparity among Indian states, with some states showing revenue growth. The inter-state disparity remains huge in FY25 BE, with most states budgeting a slower growth except Telangana, Karnataka, Jharkhand and Uttar Pradesh. Several states from the eastern and northern side – such as Himachal Pradesh, Assam, Mizoram and Meghalaya – are showing signs of slower revenue growth and have budgeted a contraction or minimal growth in their revenue receipts.

The capex conundrum

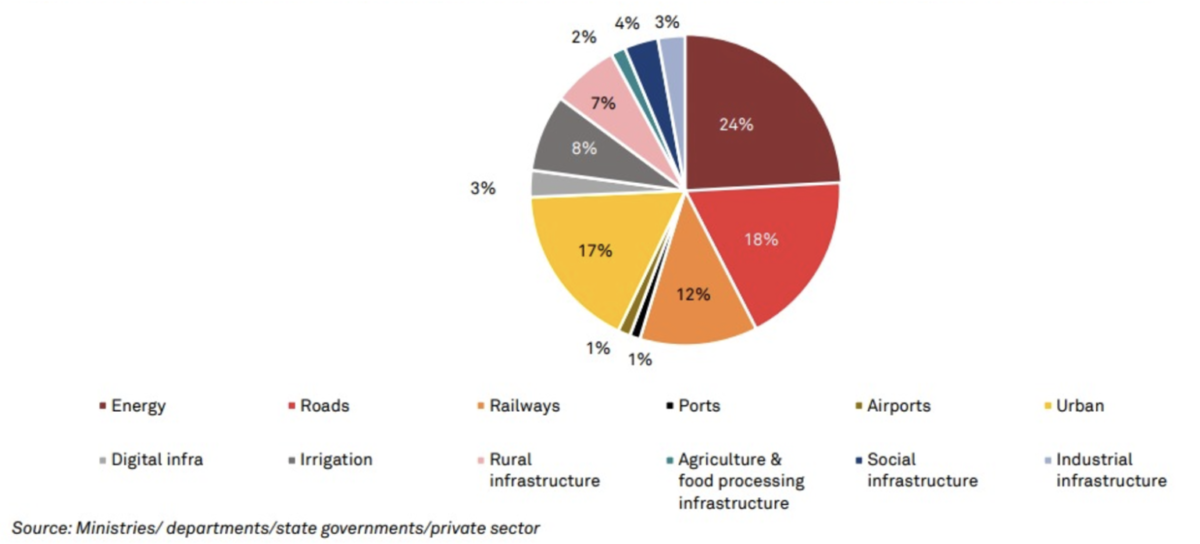

The new infrastructure thrust in India is well reflected in the heavy capex provided by the government. The National Infrastructure Pipeline chalks out an ambitious investment plan to the tune of Rs 111 lakh crore or US$ 1.4 trillion from 2020 to 2025. The plan is targeted at energy, roads, railways and urban development.

Sector-wise break-up of capital expenditure. Fiscals 2020-2025. Source: National Infrastructure Pipeline

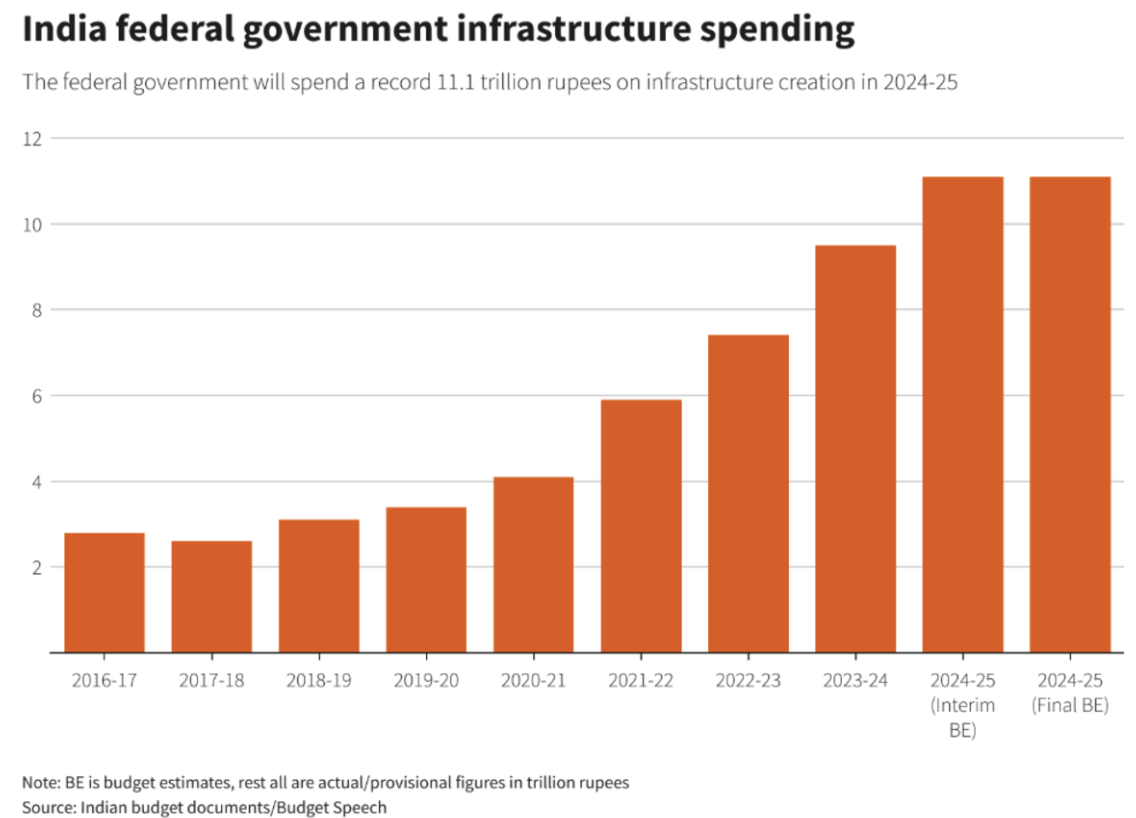

The government retained an all-time high infrastructure spending target of Rs 11.11 trillion in the fiscal year 2024-25, accounting for 3.4% of the GDP.

Despite these investments, the expected multiplier effects on employment and private investment have been few and far between. According to the National Statistics Office, the share of gross fixed capital formation (GFCF), a proxy for infrastructure investment, is likely to decline to 30.1% of GDP in FY25 from 30.8% in FY24. Growth in investment demand is also set to decelerate to 6.4% in FY25 from 9% in the previous fiscal year.

Source: Indian budget document

Above all, the creation of jobs is a source of concern. The unemployment rate according to the government was only 3.2% in the 2022-23 fiscal year, much lower than an already historically low rate of unemployment in the United States The private think-tank, Center for Monitoring Indian Economy said unemployment in May was 7.0%, up from around 6% before the pandemic, and rose to 9.2% in June 2024.

Additionally, the expected crowding-in effect on private investment has been slow. While public investment has been strong, private capital expenditure has not kept pace, raising concerns about the sustainability of growth driven predominantly by public funds. This gets more complicated on account of fiscal constraints.

Without adequately matching revenue upwards, continuing high levels of public capex risks blowing out fiscal deficits, which in turn can hurt economic stability. On top of the issues regarding finances, the biggest challenges lie in the area of implementation like delays in project approval and land acquisition.

While the improved capex and infrastructure investments in India are commendable, significant gaps in implementation, job generation and stirring of private investments have to be overcome to realise the complete potential of these investments.

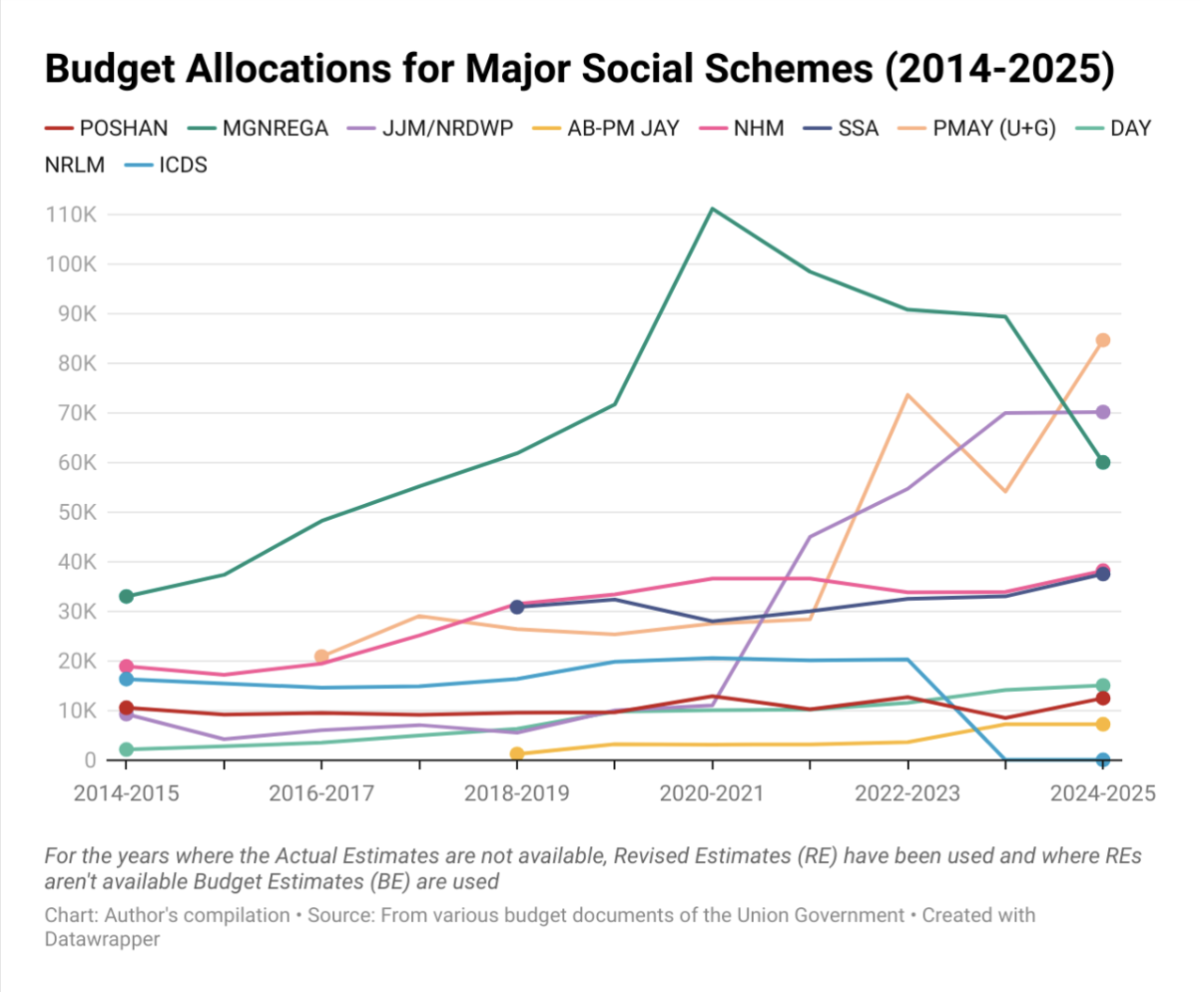

Increasing capex at the cost of welfarism

Many of the already existing social sector schemes for public and private goods, that have been there since the UPA times, have simply been renamed without any substantial justifications or changes.

The fund allocation to the schemes has remained stagnant or declined, leaving a sense of precarity among the populace eager to be included under various welfare schemes. Thomas Piketty in 1995 emphasised on the role of redistributive policies for better social mobility.

Recent data underscores the persistence of inequality, with the K-shaped recovery noted by Nomura, indicating a widening gap between high-income and low-income households. While higher-income groups are benefiting from asset appreciation and easier credit access, middle- and lower-income groups continue to grapple with high inflation and limited disposable income. This disparity has further stressed rural demand, with FMCG sales (fast moving consumer goods) in rural areas declining.

Electoral outcomes shouldn’t merely serve as a referendum on unmet promises, especially with youth unemployment at a troubling 10-13%. This reality challenges the broader narrative of “acche din,” which oscillates between potential and palpable discontent, weakening the political juggernaut and its optics-driven growth model.

On one hand, policies prioritise liberalisation, privatisation and globalisation (LPG), while on the other, public perception is managed through high-visibility projects and carefully crafted narratives. While global image management and rebranding aren’t harmful, they shouldn’t come at the cost of the immobility of its own poor.

Source: Budget estimates

Fiscal choices alone can't decide the fate of its citizenry if the political will is unsound. Exclusion will prevail in the strides of progress if the government continues to reduce allocations to critical social security schemes. Underfunding welfare schemes risks further alienating lower-income groups, especially in rural areas, where these programs act as critical safety nets.

'Churning poverty' underscores the fragility of the gains of over 18.1% of households that escaped poverty between 2011 and 2024. Over 5% of these households slipped back into poverty due to shocks such as health crises – with rising medical expenses accounting for 60% of rural indebtedness – job losses, or agricultural distress caused by erratic monsoons, IHDS data highlights,

Two full terms of the Modi government have shown how its fiscal roadmap has been limited in scope while being too heavily centred on raising capital expenditure at the cost of essential welfare spending.

Schemes for the upward mobility of all segments of the citizenry remain heavily compromised, while electorally sensitive, entitlement-based measures are often highlighted in the name of welfarism. For example, the free ration offered to 80 million people is framed as a step towards upward mobility.

In his third elected term, while there is limited change expected in the Union government’s fiscal strategy, it may be prudent for the government to realise its shortcomings. The government needs to acknowledge its own follies and undertake structural course-correction to shape a longer-term fiscal roadmap for securing development for all.

Deepanshu Mohan is a Professor of Economics, Dean, IDEAS, and Director, Centre for New Economics Studies. He is a Visiting Professor at London School of Economics and an Academic Visiting Fellow to AMES, University of Oxford.

Ankur Singh, Aditi Verma, Bliash Dey, Sarthak Ojha and Theresa Jose are all Research Assistants with the InfoSphere team of Centre for New Economics Studies (CNES).

This article went live on January fifteenth, two thousand twenty five, at twenty-one minutes past eleven in the morning.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.