A Rs 19.35 Lakh Crore Problem: CAG Report Spotlights IT Department’s Failures

“Our new Constitution is now established, and has an appearance that promises permanency; but in this world nothing can be said to be certain, except death and taxes.” Benjamin Franklin, one of the founding fathers of the US, polymath, writer, diplomat and scientist who discovered, among other things, that lightning is in fact electricity and whose visage has adorned their 100-dollar bill for more than a century, wrote this to Jean-Baptiste Le Roy, a French physicist, in 1789.

While Franklin’s remarks about impermanence in worldly affairs is an expression of popular wisdom, is certitude a defining characteristic of the taxman’s performance in our county? I am not so sure after plodding through the Comptroller and Auditor General’s (CAG) latest audit report on the performance of the Income Tax department with regard to the recovery of outstanding taxes from assessees.

On December 17 last year, when Union home minister Amit Shah’s remarks chiding the opposition for frequently raising Babasaheb Ambedkar’s name created a furore in the Rajya Sabha, his colleague in the finance ministry, Pankaj Chaudhary, quietly tabled the CAG’s 14th Report for the year 2024 in Parliament.

This 230-page report titled ‘Subject-Specific Compliance Audit on Outstanding Demand on Income Tax Assessees - Department of Revenue, Direct Taxes’ for FY 2022, has received hardly any media attention despite its shocking contents.

What is the CAG report all about?

Between November 2020-January 2023, the CAG conducted a two-phased audit of the IT department’s performance vis-à-vis raising, recording and recovering income tax demands from individuals and corporate assessees. The audit report was prepared for submission to the president in accordance with Article 151 of our Constitution. The CAG says it selected this topic because:

- An analysis of the ‘total outstanding demand’ figures (i.e., the income/corporate tax which the IT department thinks assessees ought to have paid over and above what they actually paid) exceeded the total tax collections consistently between the years 2016-2020; and

- The outstanding tax demand which the department classified as ‘difficult to recover’ was more than 97% of the total outstanding demand calculated during those years.

Apparently, the CAG had spotted this trend by analysing data contained in the Union finance ministry’s Receipt Budget for multiple years prior to the commencement of the audit.

Earlier when the CAG had audited the performance of the IT department in 2011, only 84.3% of the total outstanding demand had been categorised as unrealisable.

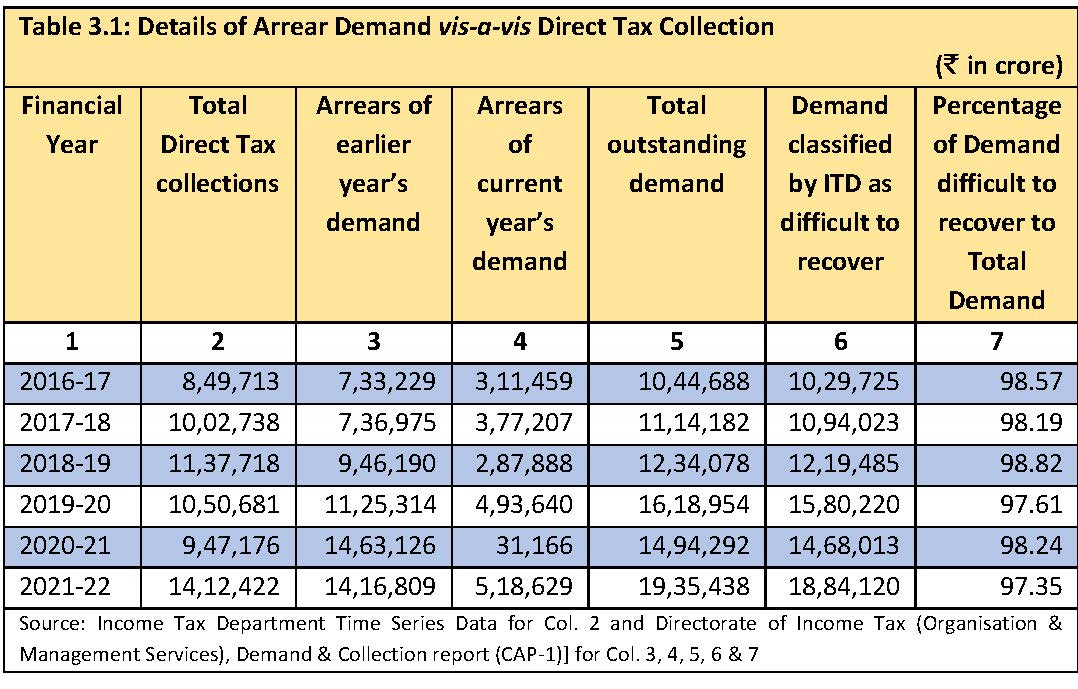

Table 3.1 which contains these figures is extracted from the CAG’s 2024 report below.

Screengrab from the CAG report.

While the total direct tax collection (income tax and corporate tax) was almost Rs 8.5 lakh crores in 2016-17, the total outstanding tax demand (including arrears from that year and previous years) was Rs 10.44 lakh crore.

By 2021-22, the total direct tax collections had increased to Rs 14.12 lakh crore but the outstanding tax demand had ballooned to Rs 19.35 lakh crore.

While the outstanding tax demand classified as ‘difficult to recover’ in 2016-17 was a little less than Rs 10.3 lakh crore, this figure had inflated by 83% to reach Rs 18.84 lakh crore in 2021-22 (details are presented towards the end of this write-up).

So the CAG commenced the latest audit to ascertain:

- Whether the targets fixed in the IT department’s central action plan to recover the tax dues and the actual achievements are adequate and in line with department’s vision 2020 document;

- Whether the tax arrears demand was properly drawn up and reported to the stakeholders and to find out the reasons for the huge outstanding amounts and analyse the reasons for the increase in volume every year;

- Whether the IT department has taken all possible action as provided in the IT Act, its Rules and the instructions of the Central Board of Direct Taxes (CBDT) for the speedy recovery of arrears; and

- Whether an adequate internal control mechanism exists to watch and pursue the recovery of dues after the demand is raised.

How well did the IT department cooperate with the CAG?

The CAG says that it had sought details of all IT assessees from whom tax demands were pending as on March 31, 2020 to select sample cases for the purpose of this audit. However, CBDT is said to have stonewalled repeated requests for the data (status up to March 2024).

The CAG then felt compelled to modify its approach. A two-tier sampling technique was used to select assessment units and corresponding Tax Recovery Officers (TROs) from the data available with CAG as of September 2017, and specific cases of assessees within the selected assessment units as on March 31, 2020.

Subsequently, the CAG requested the IT department for records of 18,870 cases with outstanding tax demand totalling Rs 7.59 lakh crore. The IT department apparently produced information about only 10,896 cases pertaining to 8,080 assessees with an outstanding tax demand of almost Rs 6 lakh crores.

The CAG noted that the IT department did not produce records of cases involving some companies with high outstanding demand and cited three companies (one of which is Delhi-based) whose demands totalled more than Rs 11,000 crore.

Readers may note that the CAG has used alphanumeric codes to identify individuals, companies and other categories of tax assessees in its report instead of naming them due to confidentiality requirements under the IT Act.

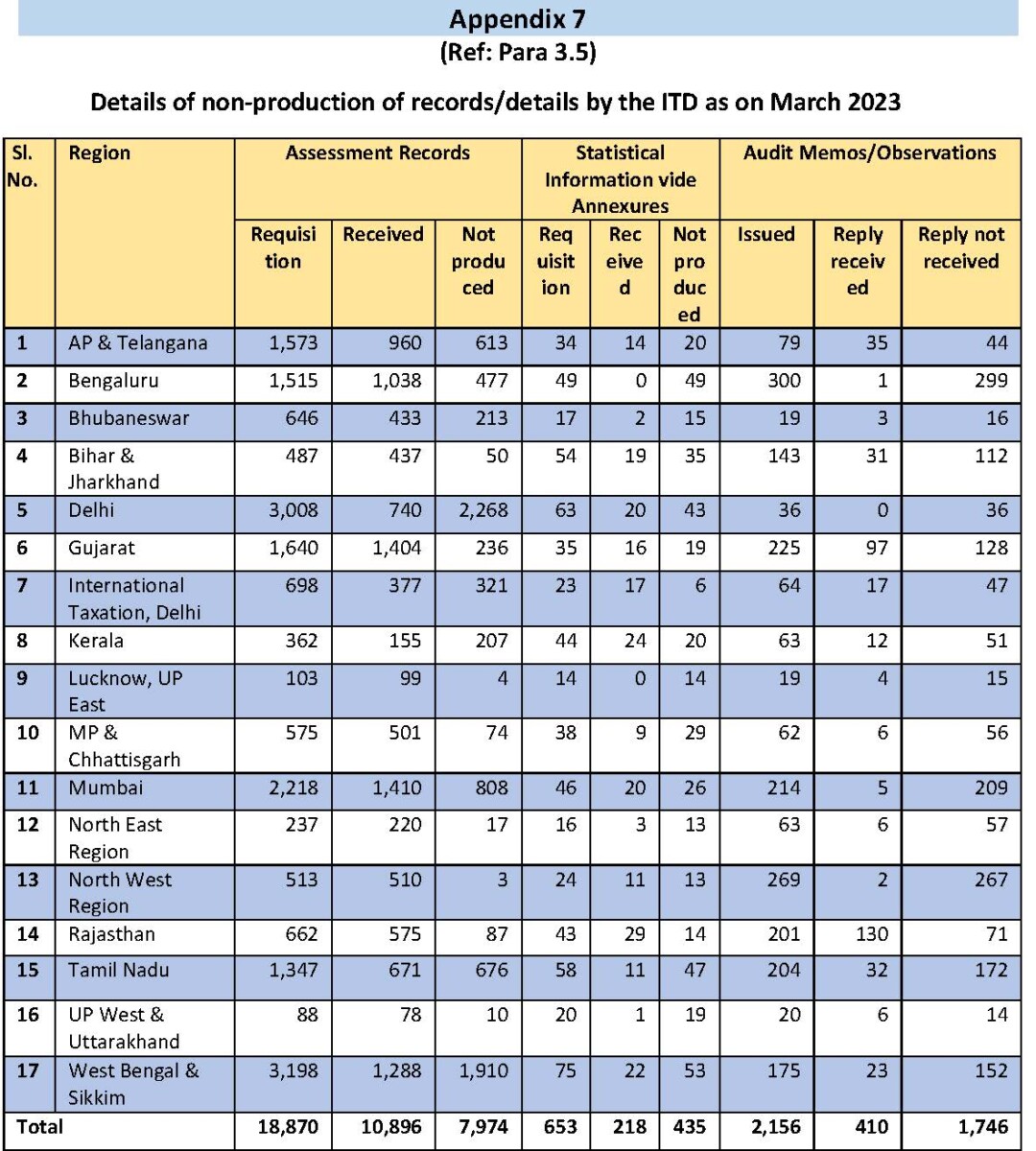

The CAG says it issued 2,156 observations/queries during the audit process but the IT department did not respond to almost 81% (1,746) of them. The region-wise figures for non-production of records/responses by the department presented in Appendix 7 are extracted from the CAG’s report below:

Screengrab from the CAG report.

The CAG’s major findings

- Outstanding tax demand vis-à-vis India’s GDP increased from 4.76% in 2016-17 to 5.88% in 2021-22 (para 4.1.3, page 25);

- While the percentage of accumulated outstanding tax demand vis-à-vis actual tax collection in the category of indirect taxes (such as GST) ranged between 16-18% per financial year during the period 2016-2021, in the direct tax category, it ranged between 86-152% during the same period (para 4.1.5, pages 26-28);

- As on March 31, 2022, cases involving outstanding income tax demand that had not been resolved for more than 10 years accounted for Rs 33,587 crore whereas those which had remained unresolved for 1-2 years accounted for Rs 8.68 lakh crore. Cases pending for 2-5 years accounted for Rs 4.44 lakh crores and Rs 44,021 crore were stuck in cases that were 5-10 years old (para 4.1.2, page 24);

- Mumbai and Delhi regions together accounted for more than half (52%) of the cases involving outstanding income tax demand followed by Gujarat accounting for 7% of the cases. West Bengal and Sikkim together accounted for 6% of the cases and Tamil Nadu, Bengaluru and Andhra Pradesh along with Telangana accounted for 5% each (para 4.1.4, pages 25-26);

- Out of the sample of 18,870 cases which the CAG selected from 279 assessment units and 74 TRO units for conducting the audit, corporate assessees i.e, companies accounted for almost 57% involving Rs 3.83 lakh crore. This is more than 50% of the volume of the outstanding demand. Individuals (excluding HUF) accounted for almost 30% of the cases involving Rs 3.13 lakh crore (para 4.2.3, pages 29-30);

- In the sampled cases, the CAG noticed that there was a 490.6% increase in the number of cases which had remained unresolved for more than ten years between March 2018-March 2020 involving an outstanding amount of more than Rs 95,000 crore. In the category of cases which had remained unresolved for 1-5 years during this period, there was a 226.7% increase involving an outstanding amount of Rs 2.15 lakh crore (para 4.2.5, page 31);

- In the sampled cases, during the period between March 2018-March 2020, there was an 84.8% increase in the number of cases involving companies (from 5,693 to 10,522) with outstanding tax demand. While the volume of tax demand for this sampled category was Rs 1.36 lakh crore in 2018, it had ballooned to Rs 2.46 lakh crore in 2020 (181.3% increase). The number of individual cases increased by almost 75% during this period (from 3,140 to 5,491 cases) accounting for Rs 77,611 crore of outstanding tax demand (33% increase) (para 4.2.6, page 32);

- In the sampled cases, as of March 2018, there were only seven cases involving an outstanding demand of more than Rs 10,000 crore each. By March 2020, there were ten such cases. There were 235 cases involving outstanding tax demand of more than Rs 100 crores but less than Rs 500 crores in March 2018 but this figure had gone up to 605 in March 2020 indicating a 157.4% increase (para 4.2.7, pages 32-33);

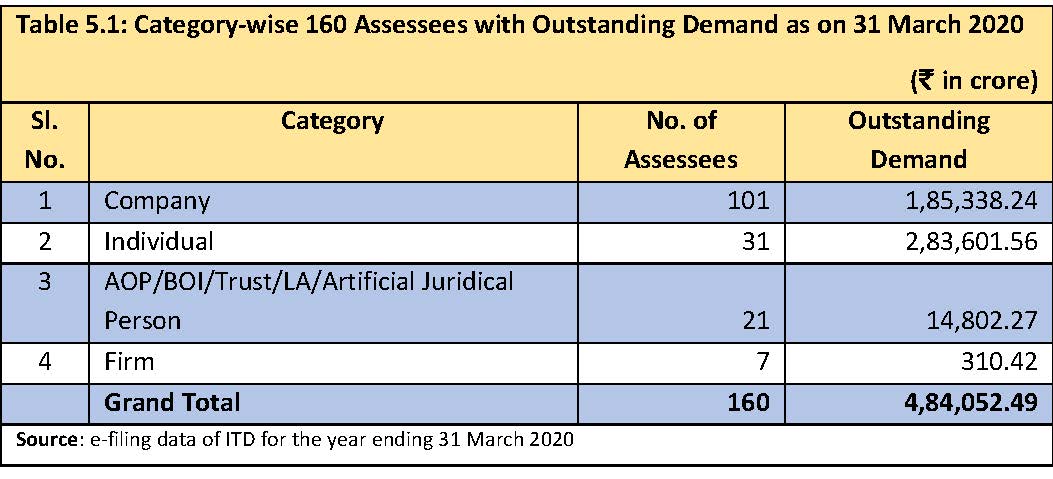

- Out of the sample selected, the CAG conducted a detailed examination of 160 cases involving an outstanding demand of Rs 4.84 lakh crores. The category type breakup of sampled cases extracted from the report is given below (para 5.2, page 36):

Screengrab from the CAG report.

- Out of the 101 corporations that CAG selected for detailed examination, six of the top ten assessees are Delhi-based, aggregating an outstanding demand of almost Rs 77,658 crores. See the amount of outstanding demand against each of these unnamed entities in the table extracted from the CAG report (para 5.2.1, page 37);

Screengrab from the CAG report.

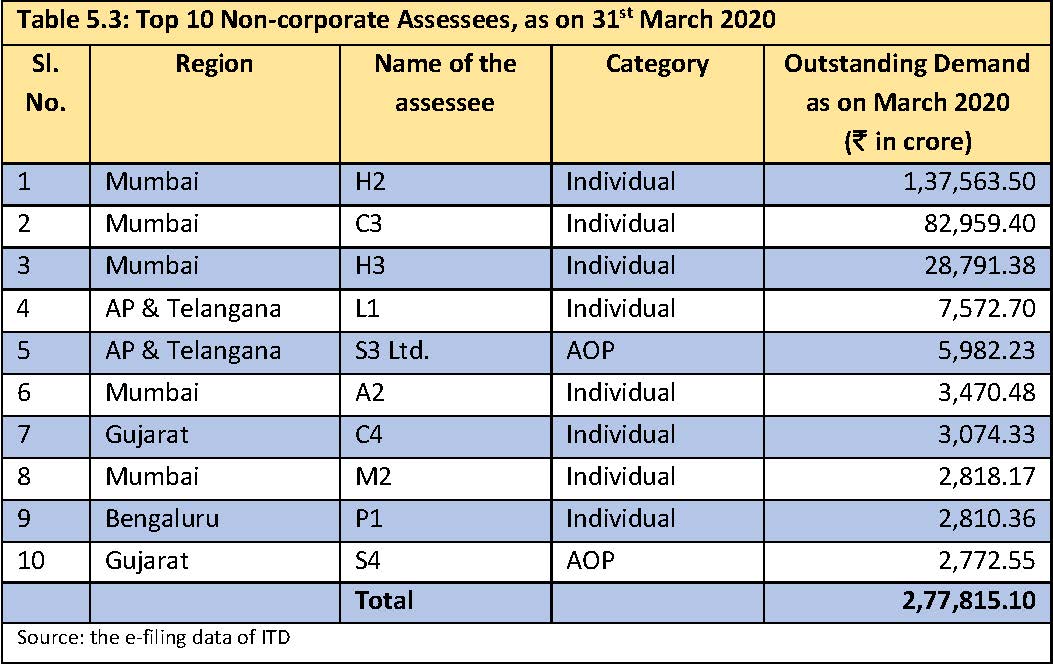

- Out of the 59 non-corporate assesses, 50% of the top ten assessees are Mumbai-based individuals aggregating an outstanding demand of almost Rs 2.56 lakh crores (para 5.2.2, pages 37-38).

Screengrab from the CAG report.

The CAG report discusses some of these cases in detail and how the IT department dealt with them. Not only is there a narration of the instances of default attributed to the assessees but also stories of the lackadaisical manner in which the IT department either handled them or failed to update its own databases even when such cases were resolved at the appeals stage.

Despite the anonymity maintained in the report, the CAG’s citation of the media-reported history of these cases makes it easy to identify the names of some of these assessees.

The CAG’s findings about IT department’s compliance failure

The CAG has also uncovered a multitude of problems with the IT department’s track record of compliance with the statutory provisions, rules, circulars and mandatory guidelines issued by the CBDT from time to time. Some major observations are summarised below:

- Non-maintenance of dossiers and faulty data: An IT Assessing Officer (AO) is vested with statutory powers to determine tax liabilities of assessees and collect outstanding demands.

The AO is required to prepare a quarterly dossier report for every defaulting assessee in order to enable monitoring of the case by the appropriate authorities. Monetary limits are fixed for this purpose from IT Range Heads to Member (Revenue), CBDT.

From the 279 sampled assessment units selected for the audit, the CAG observed that there were 42,258 assessees against whom the outstanding demand was more than Rs 30 lakh each.

When the CAG tested 5,321 cases, it found that the IT department had prepared dossiers for less than 12% cases. In 87 cases, dossiers had not been prepared and for the remaining cases (87%), ITD did not provide the CAG with dossiers despite receiving formal requests.

Some of these included high value cases mentioned in the tables displayed above. The CAG raised this matter with the IT department in June/July 2021.

Their reply was awaited as of March 2024. The audit exercise also discovered discrepancies in the maintenance of dossiers which were scrutinised. Some of these cases are discussed in detail in the report (paras 6.2.1-6.2.2, pages 89-94).

Also read: Number of CAG Reports on Centre Down by 75% Over the Last Five Years: RTI

- Raising excess tax demands: The CAG noticed instances where the IT department had raised inflated tax demands by not allowing either full credit of taxes already paid by the assessee or by delaying the implementation of orders issued in appeal by higher authorities.

The audit exercise unearthed 79 cases where the delay in giving effect to the appeal orders ranged from four days to more than seven years. There were also instances of undue levy of interest. As a result, the IT department had to refund excess demands collected along with interest causing avoidable loss of revenue to the exchequer and hardship to the assessee, the CAG noted (paras 6.2.3-6.2.4, pages 94-101). Some case studies belonging to this category are discussed in the report;

- Non-collection of requisite payment on filing appeal: CBDT’s instructions require AOs to grant stay on the tax demand when the appeal is filed if the assessee pays 15-20% of the disputed tax amount. The CAG noticed that when it checked more than 3,400 cases, assessees had paid the prescribed amount in only 382 cases. The IT department had not initiated the process of recovery of this amount in more than 1,300 cases. It also did not provide the CAG with details of action taken in 1,693 cases. The CAG has presented some case studies of this category as well (para 6.2.5, pages 102-104);

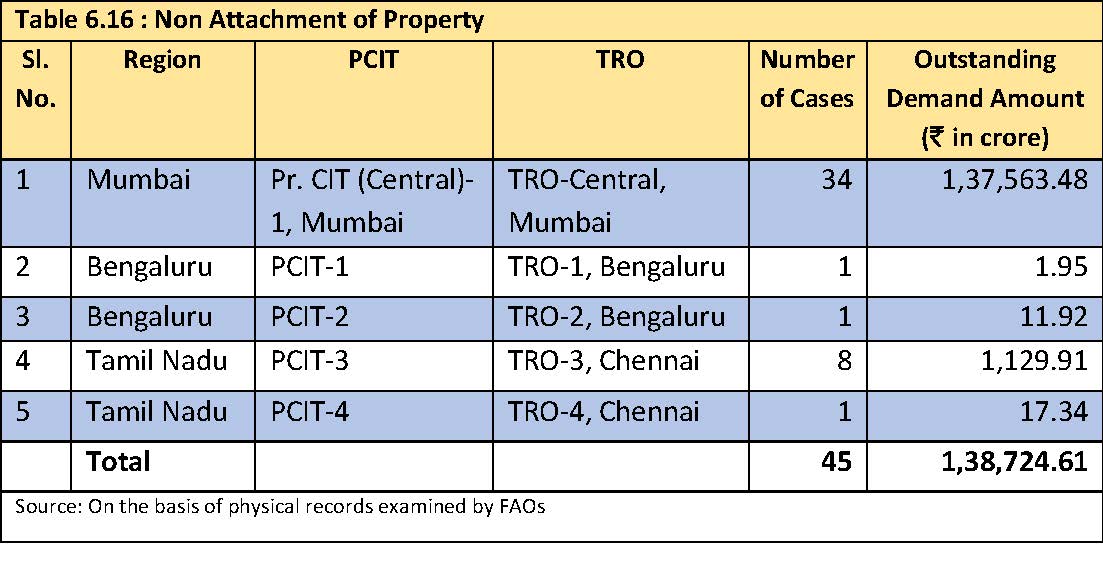

- Non-attachment of property: TROs are equipped with special powers for recovering outstanding tax demands under the IT Act. They may recover the amount by attaching the assessee’s properties, bank accounts and even arrest the defaulter.

The CAG noted that cases which it scrutinised revealed either non-attachment of property, or no further action taken to recover the amount after attachment of property, in 45 cases where the total outstanding demand was Rs 1.38 lakh crore. Region-wise details of such cases extracted from the CAG’s report are reproduced below (para 6.3.5, pages 114-116):

Screengrab from the CAG report.

- Data duplication: The CAG discovered that among the 279 sampled assessment units selected for the audit exercise, there were 7,341 duplicate cases where the IT department has raised tax demand for the same assessee, under the same section of the IT Act, for the same assessment year with the same document identification number (DIN), twice or more. This resulted in an overstatement of outstanding demand by Rs 15,652 crores, the CAG observed (para 7.2.4, pages 131-132);

- Non-levy of interest: Section 220(2) of the IT Act provides for imposing penalty on the assessee for any delay in the payment of the tax demand, interest is also applicable at the rate of 1% on the outstanding amount if not paid within 30 days. The CAG found that out of 8,965 cases tested across 11 regions, the IT department had not levied interest in almost 3,500 cases aggregating to more than Rs 69,300 crores, as of March 2021. This figure does not take into account cases where the interest leviable is less than Rs 10,000. Mumbai region alone accounted for more than Rs 43,950 crores in interest not levied for delayed payment (para 7.2.5, pages 133-135);

- Non-fixation of targets for cash collection: The CAG observed that the CBDT had set annual targets for cash collection only until 2016–17 but began setting targets for reducing arrear demand from 2017–18 onwards. So, from that year up to 2019-20, CBDT fixed the target for reduction in arrear demand at a uniform rate of 40% across all regions. However, the CAG found that no target was fixed for reduction of outstanding demand for subsequent years and achievements for the years 2019-2021 were not reported to CBDT by the regions. The CAG notes that this was primarily due to the non-reparation of full-fledged central action plans during those years (para 7.3.1, pages 138-144);

- Demand difficult to recover: As pointed out earlier, the CAG noticed that the department had characterised more than 97% of the outstanding tax demand as difficult to recover. According to the data available, “no assets or inadequate assets” of the assessee was a major contributory factor in all the years studied i.e., from 2017-2022. This factor applied to 71% of the cases in 2018-19 (para 7.3.2, pages 144-146);

- “Assessee not traceable”: This factor applied to only 12% of the cases where tax demand was deemed difficult to recover in 2017-18 but it had increased to 20% in 2021-22 (this despite the fact that some data was not made available to the CAG from the North-West Region-Chandigarh).

According to CBDT’s guidelines, the central action plan requires fixing a uniform 5% target annually for recovery of tax demand for assessees who are not traceable. However, the CAG found that the outstanding tax demand in this category more than doubled from Rs 85,337 crore in 2017-18 to almost Rs 1.78 lakh crores in 2019-20 and nearly tripled to more than Rs 2.26 lakh crores in 2021-22.

Delhi, West Bengal, Sikkim and Mumbai accounted for more than 60% of the cases across India classified as ‘difficult to recover’ because the assessees were not traceable (para 7.3.4, pages 148-149);

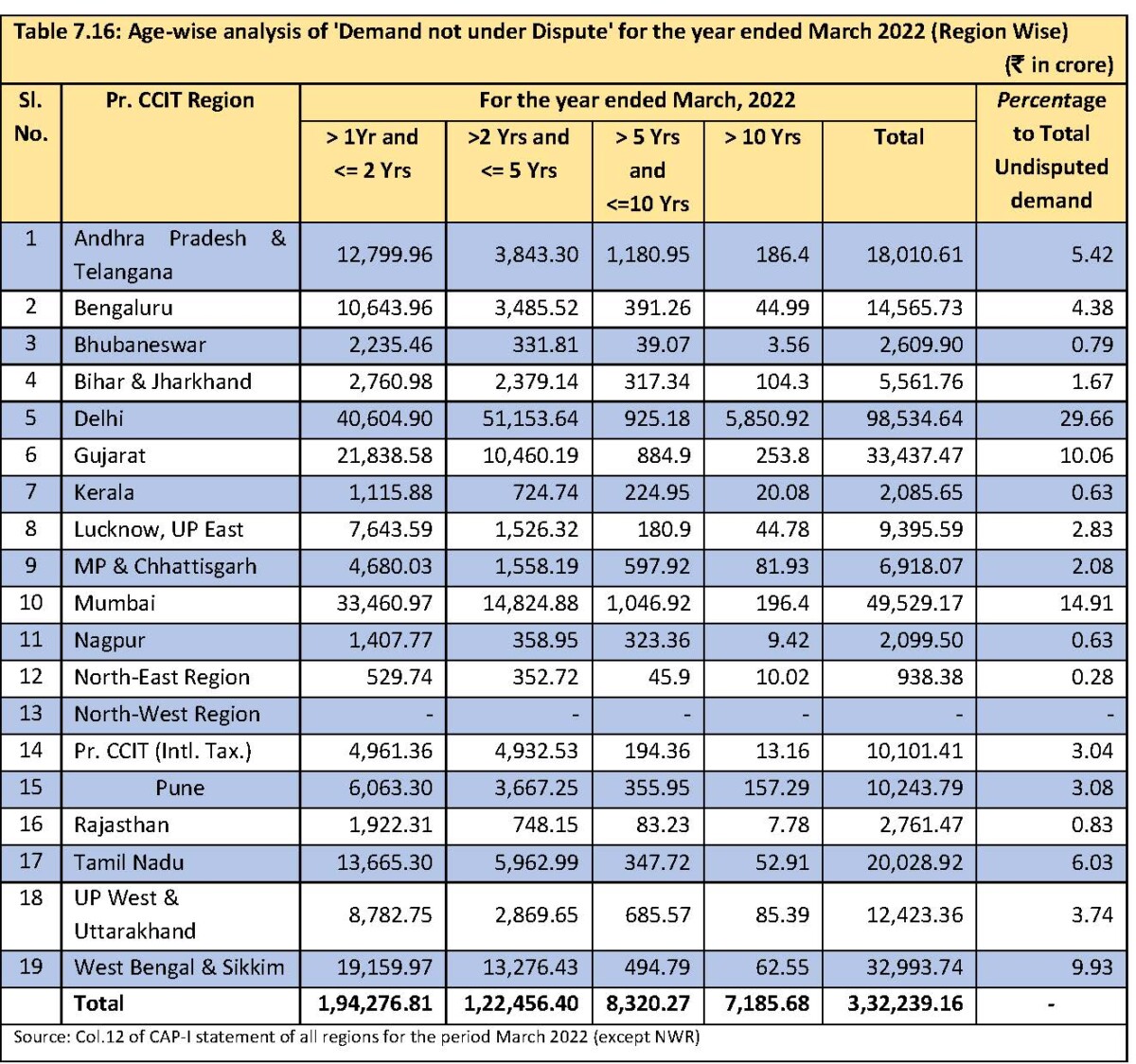

- Non-recovery of undisputed demand: The CAG found that outstanding tax demand which was undisputed (i.e., no appeal or court proceedings had been initiated by the assessees against the demand raised by ITD) amounted to Rs 3.32 lakh crore as on March 31 2022. Out of this, more than 50% i.e., Rs 1.38 lakh crore had remained unrealised for more than two years.

The region-wise data table indicating the length of time for which the IT department had let the undisputed demand amounts go unrealised is extracted from the CAG’s report and reproduced below (para 7.4, page 156):

Screengrab from the CAG report.

Unanswered questions

The CAG’s findings summarised above have a galling effect on salaried taxpayers whom the IT department chases with pre-filled online income tax returns demanding penalty and interest on tax payable which is not already deducted at source (such as interest earned on bank deposits which we get to know only after the financial year has ended).

The IT department expects us to pay advance tax to avoid such penalties and interest. But others – who are obviously high net worth individuals (HNIs) and corporates – in the public and private sector have a gala time resolving their outstanding tax demands.

The IT department is arguably one of the arms of the Union government which has digitised its work much more than others. The faceless assessment system was introduced with much fanfare in October 2019 for better and more ‘transparent’ taxpayer services and improved grievance redressal mechanisms.

Despite this, 97% of the outstanding tax demands are characterised as difficult to recover while Rs 1.38 lakh crore of undisputed tax demand remains unrealised for more than two years and Rs 2.26 lakh crores of outstanding tax demand cannot be realised because the ‘assessees are not traceable’. Truly faceless system indeed.

With these kinds of damning findings, can we really accept the elitist argument that the government cannot afford to give legal cover to the farmers’ demand for a minimum support price?

The National Talent Scholarships scheme for meritorious students which costs the exchequer barely Rs 13 crores per year has to be shelved as part of austerity measures?

Why has the social sector spending on health, education, food subsidies, fertiliser subsidies, welfare programmes for women and children and MGNREGA etc. seen either very modest increase in budgetary allocation or faced substantial cuts in recent years?

Is there insufficient money to meet the projected needs of the armed forces, given a 22% decrease when comparing allocation figures from 2015–16 to 2023–24?

This CAG report is another warning bell for taxpayers who have high expectations from the government about its ability to guide our economy to becoming the third largest in the world. I hope that the parliament’s public accounts committee will take up this report for discussion and demand explanations from the government for this terrible state of affairs.

MPs must cite from this report during the debate on the motion of thanks for the President’s address next month and the subsequent debate on the budgetary proposals that the Union finance minister will present for 2025-26. The whistleblower in this case is a constitutional authority, not a ‘disgruntled’ government official or a ‘busybody RTI activist’.

Banks’ non-performing assets and loan write-offs dominated public discourse last year but not enough is being said about tax defaulters.

Given the primary role of public and private corporations and HNIs in the tax demand arrears that have accumulated, it is high time that their identities are made public – especially those ‘assessees who cannot be traced’ or whose assets cannot be seized.

Irrespective of the extra protection from the Digital Personal Data Protection Act, 2023, which the IT department will use to deny access to such information, if adequate citizen pressure is mounted, the publication of this data can be compelled on grounds of immense public interest. A beginning can be made by filing RTI applications with the IT department in large numbers.

Venkatesh Nayak is Director, Commonwealth Human Rights Initiative, New Delhi. All facts are in the public domain, views are personal.

This article went live on January twenty-eighth, two thousand twenty five, at thirty minutes past four in the afternoon.The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.